Loading...

Budget Hearings - DWSD, Office of Auditor General

Speaker 1

grass removed as is why not all right? Since 2010 That's right number 605 097 to provide Recreation and Park renovation at Dexter Elmhurst Community Center contractor apply plus Inc, located at 219 North Main Street, Ann Arbor, Michigan 4810 for a contract period upon city council approval through December 31 2020 for total contract amount $694,700 Is there a motion to move Lando? Six points in the formal session with recommendation for approval to be put on to new business?

Unknown Speaker

Discussion this guy should

Unknown Speaker

chair recognizes member callow vice chairwoman catalyst.

Speaker 2

Thank you. I'm sure this will get voted up but it's so unfortunate that we weren't able to find a local company. This is 690 $400,000 going to Ann Arbor using Arper dollars. And it's just so unfortunate every time I see this with these numbers of dollars going to suburban, Metro Detroit, it's just it's just disturbing to me so I know I'll be a no vote. On this. But there's no way you can't tell me that you could not find a company based in Detroit minority or women on to do this work because we've been seeing over and over again where these wrecks were these recreation department these parks and recreation facilities have had Detroit based companies work on them. And so this is the Dexter Elmhurst Community Center brand new build out and it's just concerning to me that we always seem to find ourselves going outside of the city to do work that I know we desperately need to keep in the city supporting minority and women owned businesses. But again, you know, it'll probably get approved without my support. Thank you, Mr. Chair.

Speaker 1

What was that was that was Gerald Stabler. Were you directing at anybody? Are you? Okay, that's interesting. Did you want to say something to that or

Speaker 3

do the chair I would just say that we only received to be it for this and this company based in Ann Arbor, came in at the lowest and most responsible and capable of doing the work. We have been working closely with OCP to diversify our vendors and condors rarely hosting events ourself amongst our team to help with vendor recruitment and things of that nature. And so we do understand that this is an ongoing issue and we definitely are attempting to prioritize different based businesses.

Speaker 1

You want to I was gonna ask you miss Henderson sees you it's see I'm seeing here you invited 64 suppliers do you have a percentage of how many those were Detroiters?

Speaker 3

May have to fire to OCP on that one. I do not have that information. Sure. Yes.

Speaker 1

We do have Eric Cooper is listed as Cooper II. Okay, Mr. Cooper floor is yours. And with the clerk note that we have been joined by member waters.

Unknown Speaker

The clerk window

Unknown Speaker

Thank you, Madam Clerk. What about you the big bucks.

Unknown Speaker

Good afternoon. As it relates to the question of the

Unknown Speaker

model. Mr. Cooper, can I see your face man?

Unknown Speaker

I'm sorry, please.

Unknown Speaker

Thank you, brother. Just kind of creeps me out. Go ahead.

Speaker 4

Go everyone. As it relates to the amount of Detroiters that were a part of the bid. That is some information I will forward to you that get that to you.

Speaker 1

Excellent. Appreciate it. To recognize the number cattle vice chairwoman Katelyn,

Speaker 2

Mr. Chair since we have him on the line is there any way some of this work could be subcontract subcontracted out to minority and women business contractors in the city of Detroit? These are 100% Awkward dollars that black folks qualify for the city to get. Can we get a little bit of it? It seems to always go outside of Detroit. We get a little bit. Can we get contractors,

Speaker 4

as Hindus as Natalia was reiterating a little earlier. We're definitely working on that and trying to provide opportunities where there's collaborations for those subcontractors.

Speaker 1

All right, thank you, sir. I appreciate it. Okay. Well, thank you man for that man. Thanks. Very Excuse me. Vice here. Good Lord. All right. Is there a motion to move line item six points in the formal said with recommendation for approval to be put on to new business are your judges here in line I know six point team will be moved on to formal session with recommendation for approval to be put on to new business will often line item six point 11 Contract Number 605 131 100%. capital funding to provide stoep old number one park improvements contractor Michigan recreational construction location 18631 Coney, detroit michigan 48234. contract period upon city council approval February 28 2020 for total contract amount of $500,000. Is there a motion to move line item six point 11 The formal session with recommendation for approval we put on to new business or any objections Hearing none line on six point 11 We put onto formal suit will move to formal session with recommendation for approval to be put onto new business line oh six point 12 Contract Number 605 135 pt per se bond 38 Proceed capital 12% grant funding to provide Irma Kinder seed Marina design engineering services contractor Smith Group Inc location five degrees Wall Street Suite 700 Detroit Michigan 48226 contract period upon city council approval through June 30 2020 for total contract amount $650,000. Is there a motion to move 906 points well the formal session with recommendation for approval to be put on to new business multidomain Are there any objections? Hearing none line on six point 12. We move to formal session with recommendation for approval to be put on to new business will the quarter please note that we've been joined by men and President Mary Sheffield

Unknown Speaker

The clerk will no

Speaker 1

lie no six point 13 Contract Number 605 130 100 Proceed capital funding to provide a new dog park at Palmer Park contractor Michigan recreational construction location 186 31 COVID Detroit Michigan 48234 contract period upon city council approval through February 28 2020. For total contract amount $500,000. Is there a motion to move line item six point 13 The formal session with recommendation for approval to be put on to new business? motion has been made. Are there any objections? Hearing none line oh six point 30 Who put on the formal session with recommendation for approval be put on to new business line item six point 14 The approval innovation to commit $150,000 To the city contribution to support the Detroit Wayne County Port Authority in the installation of an additional bollard along the Detroit Riverwalk. The General Services Department hereby requests the approval and authorization from your honorable body to commit $150,000 The city contribution to the Port Authority to construct an additional bollard servicing cruise ships that dock along the riverwalk the bollard the bollard will be installed in the portion of the riverwalk in front of the Renaissance Center. The primary purpose of the bollard project is to upgrade facilities in order to accommodate large cruise ships, particularly cruise chutes brought to Detroit Detroit by Viking Cruises which are 200 feet longer than any other cruise ship entering the Great Lakes. Now I think we have people who are on Is there a motion to discuss line or since 2014 motion I think we have missed the culture art for Freeman.

Unknown Speaker

Excuse me for interrupting.

Speaker 1

Go ahead, miss. Go ahead. Dr. Powell. I know you come in sooner or later.

Speaker 5

Well, I've been trying to give you a couple of minutes. President needs to call the two o'clock meeting and then so you're gonna have to, you know, wrap it up

Speaker 1

or wait, I know it was a borrowed time. I knew it. I knew it. I knew you were coming for me. It's okay. All good. So I'm just advising. I understand, just tell me what to do here.

Speaker 5

Well, at this point, you should at least recess to the call of the chair. Let the President call the two o'clock meeting and then go back into your meeting to wrap it up. Because it's already what 10 After the hour 11 after.

Speaker 1

Okay. So what you want to do, man president, we've probably reset that and you can finish your committee. Okay. The neighborhood committee services committee now students at recess is called

President Sheffield

Pocket worthy expanded budget financial party committee if a clerk will call the roll.

Unknown Speaker

Councilmember Scott Benson.

Unknown Speaker

Benson, aye.

Unknown Speaker

Councilmember Fred dr. Hall, the third present. Councilmember Leticia Johnson, Councilmember Gabriela Santiago Romero. Councilmember Mary waters. Councilmember Angela Whitfield Callaway present. Councilmember Coleman a young the second here, Councilman. I'm sorry, council president pro tem James che. Council President Mary scheffau. President. Madam President, you have a quorum.

President Sheffield

Thank you. Thank you. We will stand in recess. To the call of the chair.

Speaker 1

All right. Neighborhood certain neighborhood a community service Study Committee is now in starting with the clerk please call the roll. Am I doing that right that the powers okay.

Speaker 5

Yes, sir. You're back in session in the clerk will call the roll.

Speaker 1

Okay, he's looking at me. I just wanna make sure all right. I'm sorry. I was okay. I just I just wanna make sure you use give me their face and I make sure I'm doing it right. I won't be on the wrong side. All right. Thank you. Appreciate you love you. All right. Well, we do without you. All right, um, but we please call the roll.

Speaker 6

Councilmember Coleman again, the second councilmember Angela with Callaway.

Speaker 6

Councilmember Angela Whitfield Callaway present. Oh, good. Counsel, Mr. Robinson,

Unknown Speaker

I've been tonight.

Unknown Speaker

Mr. Clark, you I'm sorry, Mr. Chair. You have a quorum present.

Speaker 1

All right. Thank you, Madam Clerk. Appreciate you. Alright. We're at 614. Mr. Lockhart is the person that's here to speak to line item 614. Mr. Lockhart, sir.

Unknown Speaker

floor is yours. Motion to discuss.

Speaker 1

We've already made that motion. Yeah, when there was. Motion is mostly made or any objections? Motion is guest through the Chair. Mr. Lockhart my man. Go ahead.

Speaker 7

Hey, how's it going? On time, I'll just kind of give a quick overview. I know you already had mentioned yesterday requesting $150,000 from a city contribution to put together with Wayne County's $150,000 Another $50,000 coming in through the Port Authority Viking cruise and the pilot association to construct a bollard on the Detroit Riverwalk in front of the Renaissance building.

Speaker 1

Excellent Am I also any questions? Chair recognizes vice chairwoman Ken Oliver. Oh, no way he left. All right. Chair recognizes vice chairwoman Callaway.

Speaker 2

Thank you, Mr. Chair. Just a real quick question. Are the bollards going to be insured? just hypothetically If the cruise ships happened to damage the boilers who's responsible? Would it be Wayne County us? Or would the responsibility be on the cruise ship?

Speaker 7

Through the Chair, I'll have to follow up with that question. With law in the Port Authority I know we have Mark from the port authority on this call if we can add him to speak.

Unknown Speaker

All right, what was Mark last name?

Unknown Speaker

Trump sch Mr.

Speaker 1

Trump oh yeah mr. travel trip. Mr. shrub. floor is yours just have the need for speed sir. times of the Essence All right.

Speaker 8

I heard the question and liability for any damage that would be caused when a ship ties off on the bollard. We would have insurance. The port authorities insurance would cover our our own liability. We also have an engineer errors and omissions policy that would cover if if if the bollard was designed in properly or the contractor installed it properly we would have their insurance. General Motors is going to require all of that from the port authority because this bollard is going on to their property. And then if the if the ship company performs, operates the bollard improperly or doesn't tie off when they're pulling away. They would be liable to all parties as well.

Speaker 1

All right, but is that is as Okay, Chair recognizes member Benson. Alright.

Speaker 9

Thank you. And this is the question I had during the port authority budget hearing the other day. What's the ROI on this extraordinarily expensive bollard? What are we getting back and see the short I see that our contribution is $150,000. But what's coming back to the city as as a form of economic development, what do we get? Yeah.

Speaker 7

I can speak to it and Mark and I can jump in the anticipated economic growth were expected as around 12,000 passengers to climb into Detroit in 2023 in at least that number annually moving forward for the foreseeable future, with a center participating in around $125 of local spending per passenger, which amounts to around $1.5 million dollars per year in local impact. And I know Mark can speak more to it but they are commissioned in the economic impact study, which is apparently on his way.

Unknown Speaker

Okay, and so when is that study going to be completed?

Speaker 8

That should be done by mid summer. Where the the impact study will cover both our cruise dock as well as the cargo operations through the port of Detroit.

Speaker 9

Okay, good. I see that we have others who are matching and I'm not. I don't I do support this type of economic development. We want to make sure that we're getting a reasonable return on our investment. One thing I did not see was the source of funds for $130,000.

Speaker 7

Yeah, so I can speak through the source would come through GSD not from Parks but from facilities so similar to some of the precincts fire station service yards. This would not take away from any current facilities but this represents the excess of availability that the GSD department has to support this

Speaker 9

GSD had a budget surplus when it comes to facilities they have too much money to wrap this

Unknown Speaker

up, we can be on the clock.

Speaker 7

So this is what they suggested as a where we have money available to conduct this activity.

Speaker 9

Okay, so I was just about there being some type of opportunity costs. I mean, we can bring this back and

Speaker 1

keep trying to wrap it up. You got we gotta wrap back in the weeds. The last question we gotta go. Go ahead. Go ahead. Go ask the question. And we move on. Oh, go ahead.

Unknown Speaker

I'm sorry. I didn't hear another question.

Unknown Speaker

To ask it again,

Speaker 9

the opportunity costs so the $150,000 If there's no surplus in GSA mean, something's not going to get done or something's not going to get repaired unless we were just in the habit of putting an extra $150,000 into GSEs budget, but I don't think that we are.

Speaker 7

Understood, I would ask that we come back to that question. Unless we have someone from our CFO that can GSD that can not only provide clear more clarity on the $150,000

Unknown Speaker

Mr. chairs or time sensitivity to this request.

Speaker 1

Well, you know, I want to move this out. Now I see the economic development opportunities. But if you want to bring this back for a week we could do that. Motion. Is there is it I'm sorry, through Is there a time sensitivity.

Speaker 8

Viking is scheduled to arrive on May 1 And we've been working to try to one get a better price for three months now. And the sooner we can let this contract move forward. The sooner we can get this done if if the bollard isn't in place, Viking will be arriving at our cargo dock.

Speaker 1

I guarantee we will get this done is land this plane before that date. Yes, my promise.

Speaker 8

So no no, we need we need the contractor to get started. So it'll take probably the full two months to get the work done. Okay,

Speaker 2

Mr. Chair? Yes, I'm motion to bring this back in a week.

Speaker 1

Okay, motion has been made. Already. Objections. Objection. One, the as avid. We will bring this item back in one week. All right. Moving on to a walk on that has been brought before us. This is an authorization to submit a grant application to the Michigan Department of Natural Resources for fiscal year 2023 Trust Fund grant. The General Services Department is hereby requesting authorization from Detroit City Council to submit a grant application to the Michigan Department of Natural Resources for fiscal year 2023 Trust Fund grant for the Eliza Howe Park. The amount being sought is $300,000. The state share is 50% or $300,000 of the requested amount and there is a recap there is a required cash match of 50% or $300,000. total project cost is $600,000. The fiscal year 2023 Trust Fund grant first full year will enable the department to construct a new nature focused playground for Eliza Howe Park, which includes connecting the place base to the natural elements in the park. If the application is approved, a cash match will be provided from appropriation to 0507 we respectfully request your approval to submit the grant application by adopting the attached resolution is there any quick motion discuss most of these guys yeah motion Are you okay hearing Okay, Chair recognizes

Unknown Speaker

Excuse me, Mr. Chair.

Unknown Speaker

Dr. Brown what I do?

Speaker 5

I'm sorry, sir. But you need a motion to walk it on first and then you can discuss it.

Speaker 1

Excellent, my bad. Thank you. Is there a motion to walk? Most of them may or any objections? Hearing none. This will be walked on to the agenda. Chair recognize these wait Now is there a motion to discuss motion? There are no objections. We will now discuss this walk on Item chair recognizes vice chairwoman Callaway.

Speaker 2

Thank you so much Mr. Chair. We've maybe a week and a half to to do this. This application is now due April. The first so it always makes me nervous when we I'm not saying we did anything at the last minute but you'd have about a week and a half, maybe two weeks to get this application in so it just be nice to not always be behind the eight ball when we have these things come before the council. So I don't know how long you've known about the contract ma'am through the chair. But you have up until April 1 I know you know the hard deadlines to send that document but you know, I don't know why we don't want to stay wait to the last minute but why do we perhaps wait to the last minute

Unknown Speaker

Sanderson go ahead and

Speaker 3

do the chair. I will be brief. I would just say that this was held by counsel. Well, it was in discussion it should have been moved with the other grants that we had earlier in the agenda. They are very similar, but it was held by potentate just because we needed to do some community engagement beforehand. And at the time person paid did not believe that we had done sufficient community engagement. So we took that back to the community members for feedback. And so that is why it was being delayed.

Unknown Speaker

Thank you. Thank you Mr. Chair. Thank you, ma'am.

Speaker 1

Is there a motion to take up this walk on item? Any objections? Wait, hold on. I'm sorry. That's the proper vote. Is there a motion to move this walk on item to issue with recommendation for approval to be put on to new business? Or the objections? Hearing none. This walk on item will be moved to formal session with recommendation for approval to be put on to new now this is a matter granted because I like to talk but is there a motion to suspend the member reports most of the made our new judges? Wait. All right. Hearing none middle reports will be suspended. Without objection. This committee is now at whoa wait a minute. Okay. Right at the buzzer. Go ahead, sir.

Speaker 9

I was told there may be someone who GSD was able to answer a question. I understand that maybe somebody from GSD who's available to answer the question regarding the bollard and the $100,000 budget item.

Unknown Speaker

Mr. Washington oh wait, I'm sorry. I missed this. I spoke to some miss Henderson.

Speaker 3

Yeah, yes. The question I believe from earlier was about the funding and if there was a surplus, I cannot speak to the surplus in our budget. It is coming out of our capital funds. If we were to do a project would come out of our capital budget. So any other questions? I can submit a writing or I could submit responses in writing just so that we can get this moved along and not miss out on this opportunity or push this timeline.

Unknown Speaker

Alright, thank you for that. All right there Benson Does that satisfy you? We'll go ahead. We got to keep it moving. So I predict

Speaker 9

going reconsider the vote on the bottle I think is 614. That's 614. There's 14.

Speaker 1

Motion to reconsider. We weren't we already pretty bad for one week. reconsider that. You want to request. Oh, you're okay. Motion reconsider? Is there a motion as a multidomain are the objections? Hearing none, we will now reconsider line item six point 14. Is there a motion to move lotto six point 14 The formal session with rubbish?

Speaker 5

Excuse me, sir, what I do. Now you have to vote on whether or not to bring it back in one week, because that's the motion you're reconsidering. So you'll have you need a motion to bring it back in one week and then that motion would be voted down and then you would get the motion to send it to formal new business.

Speaker 1

Okay, thank you Dr. Powers. Yes, sir. Is there a motion to bring back line item six point 14 Well, we already have motion, right.

Unknown Speaker

Object right.

Speaker 1

Object. Okay, that fails. So now

Speaker 9

motion to settle item 614. To formal session, new business. The recommendation to approve.

Speaker 1

Both has been made or made any objections? Hearing ly no six point 14 will be moved to formal session with recommendation for approval to be put onto new business. Mr. Chair? Yes, because we moved to adjourn. Why

Speaker 9

it's critical that the administration and those who are asking for contracts will be approved be prepared to answer all questions and have the forethought to prepare for questions that they think may be answered. And as people like to say, this is not a rubber stamp. They have to do their jobs and we have to do our job as well. So please be prepared to answer questions when it comes to how we spend the people's money.

Speaker 1

I'll say sir, without objection neighborhoods to be started standing committee is now adjourned.

President Sheffield

All right. We're gonna call back to order the expanded budget Finance and Audit standing committee for the purposes of our fiscal year 24 budget hearings. Madam Clerk, if you can please call the roll.

Unknown Speaker

Councilmember Scott Benson. Councilmember Fred R Hall, the third present. Councilmember Leticia Johnson present councilmember Gabrielle Rivero present. Councilmember Mary waters resident councilmember excuse me, Councilmember Angela Whitfield Callaway, Councilmember Coleman, a young second. Council President Pro Tem James Tate. Council President Mary chef Phil, President. You have a car Madam President.

President Sheffield

Thank you there being a quorum. We are in session and we are going to proceed with our budget hearing for the Detroit water and sewage department. We have director brown with this other representatives you can join us at the table.

President Sheffield

Director brown whenever you are ready to proceed, the floor is yours.

Speaker 10

Oh, thank you. Thank you for the opportunity to proceed. To my left is Tiffany Jones. She has nothing to do with the budget. She is my diversity and inclusion officer. It's her job to find Detroit based businesses and get them under contract along with creating opportunity. When I came before you before I told you that we'd be hiring, as well as finding 40 or 50 new fsts to do lead service and it's our job to make sure that they're Detroiters. It's her job to make sure that the contractors when she goes out to check the jobs have Detroiters on those jobs. So I just wanted you to put a face with Miss Tiffany Jones, the new versity and inclusion director so that you know that we are are doing what we said we would do. I'll let my financial team introduce themselves and then I'll let you know who's on on the Zoom call today in case this question is for them.

Speaker 11

Good afternoon, council members. Good afternoon, Madam President. My name is Tucker Raman. I'm the Chief Financial Officer of DWSD.

Unknown Speaker

And here's Michelle Williamson, budget manager

Speaker 10

and I'm gonna make sure that my financial team use their their outdoor voices so that you can you can hear them loud and clear that their finance people get used to being in a room crunching numbers but they're gonna use the outside voice today. On on the line on on Zoom calls. We also have Sam Smalley. He's our Chief Operating Officer. We have Matt Phillips, our Chief of Staff, my chief of staff Deborah pi Spiess, General Counsel, as well as Lisa Wallach who's in charge of stormwater and permit the permit process, if any questions come up  regarding those issues, we have them available. Okay, so budget considerations DWSD executive team considers these factors in developing the budget. Affordability, number one, everything that I do, I have to take into consideration how it's going to affect ratepayers and how affordable is it to do it? We want to keep rate rate increases below 4% and support water conservation initiatives. It's number one, secondly, compassionate and responsive customer service. Number three operations that support and preserve preserve public health, meet or exceed all federal, state and local regulations. Number four, employee and asset safety number five water and sewer upgrades including lead service line replacement and number five point number six, employee focus training, retention and recruitment. That's what I ask every member of my team to take into consideration when they're submitting their portion of the budget for consideration current budget environment this is extremely important. The proposed FY 2024 budget was developed in an inflationary environment with inflation rates at 6.4% for the 12 months ending January 2023, according to US labor department data, and you know, I'm happy to say that over the last eight years we've averaged rate increases of 2.84% well below the 4% and even below 3% And that's in a high inflationary environment. Even in this environment, the goal was to keep the rates affordable and at the same time not compromise on service level initiatives. The budget incorporates expenditures required to operate DWSD the water and sewer for fiscal year 2024. These expenditures become the basis for determining the revenue that are required to fund those expenditures and are termed as revenue requirements. The budget proposal proposes a 3.2 increase in rate revenue and overall revenue requirement decrease of 2% for the system as a whole. overall revenue requirement decrease is primarily due to savings of $35.4 million in pension costs due to expire the expiration of the pension agreement with the city of Detroit effect of fiscal year 24. The Rec Department expenses are projected to increase primarily due to increases in personnel cost for adding new positions to the budget necessary to support DWSD strategic initiatives. DWSD will begin average winner consumption methodology to cap sewer usage for residential customers starting in fiscal year 24. I'll let our CFO continue with the presentation.

regarding those issues, we have them available. Okay, so budget considerations DWSD executive team considers these factors in developing the budget. Affordability, number one, everything that I do, I have to take into consideration how it's going to affect ratepayers and how affordable is it to do it? We want to keep rate rate increases below 4% and support water conservation initiatives. It's number one, secondly, compassionate and responsive customer service. Number three operations that support and preserve preserve public health, meet or exceed all federal, state and local regulations. Number four, employee and asset safety number five water and sewer upgrades including lead service line replacement and number five point number six, employee focus training, retention and recruitment. That's what I ask every member of my team to take into consideration when they're submitting their portion of the budget for consideration current budget environment this is extremely important. The proposed FY 2024 budget was developed in an inflationary environment with inflation rates at 6.4% for the 12 months ending January 2023, according to US labor department data, and you know, I'm happy to say that over the last eight years we've averaged rate increases of 2.84% well below the 4% and even below 3% And that's in a high inflationary environment. Even in this environment, the goal was to keep the rates affordable and at the same time not compromise on service level initiatives. The budget incorporates expenditures required to operate DWSD the water and sewer for fiscal year 2024. These expenditures become the basis for determining the revenue that are required to fund those expenditures and are termed as revenue requirements. The budget proposal proposes a 3.2 increase in rate revenue and overall revenue requirement decrease of 2% for the system as a whole. overall revenue requirement decrease is primarily due to savings of $35.4 million in pension costs due to expire the expiration of the pension agreement with the city of Detroit effect of fiscal year 24. The Rec Department expenses are projected to increase primarily due to increases in personnel cost for adding new positions to the budget necessary to support DWSD strategic initiatives. DWSD will begin average winner consumption methodology to cap sewer usage for residential customers starting in fiscal year 24. I'll let our CFO continue with the presentation.

+1

regarding those issues, we have them available. Okay, so budget considerations DWSD executive team considers these factors in developing the budget. Affordability, number one, everything that I do, I have to take into consideration how it's going to affect ratepayers and how affordable is it to do it? We want to keep rate rate increases below 4% and support water conservation initiatives. It's number one, secondly, compassionate and responsive customer service. Number three operations that support and preserve preserve public health, meet or exceed all federal, state and local regulations. Number four, employee and asset safety number five water and sewer upgrades including lead service line replacement and number five point number six, employee focus training, retention and recruitment. That's what I ask every member of my team to take into consideration when they're submitting their portion of the budget for consideration current budget environment this is extremely important. The proposed FY 2024 budget was developed in an inflationary environment with inflation rates at 6.4% for the 12 months ending January 2023, according to US labor department data, and you know, I'm happy to say that over the last eight years we've averaged rate increases of 2.84% well below the 4% and even below 3% And that's in a high inflationary environment. Even in this environment, the goal was to keep the rates affordable and at the same time not compromise on service level initiatives. The budget incorporates expenditures required to operate DWSD the water and sewer for fiscal year 2024. These expenditures become the basis for determining the revenue that are required to fund those expenditures and are termed as revenue requirements. The budget proposal proposes a 3.2 increase in rate revenue and overall revenue requirement decrease of 2% for the system as a whole. overall revenue requirement decrease is primarily due to savings of $35.4 million in pension costs due to expire the expiration of the pension agreement with the city of Detroit effect of fiscal year 24. The Rec Department expenses are projected to increase primarily due to increases in personnel cost for adding new positions to the budget necessary to support DWSD strategic initiatives. DWSD will begin average winner consumption methodology to cap sewer usage for residential customers starting in fiscal year 24. I'll let our CFO continue with the presentation. Speaker 11

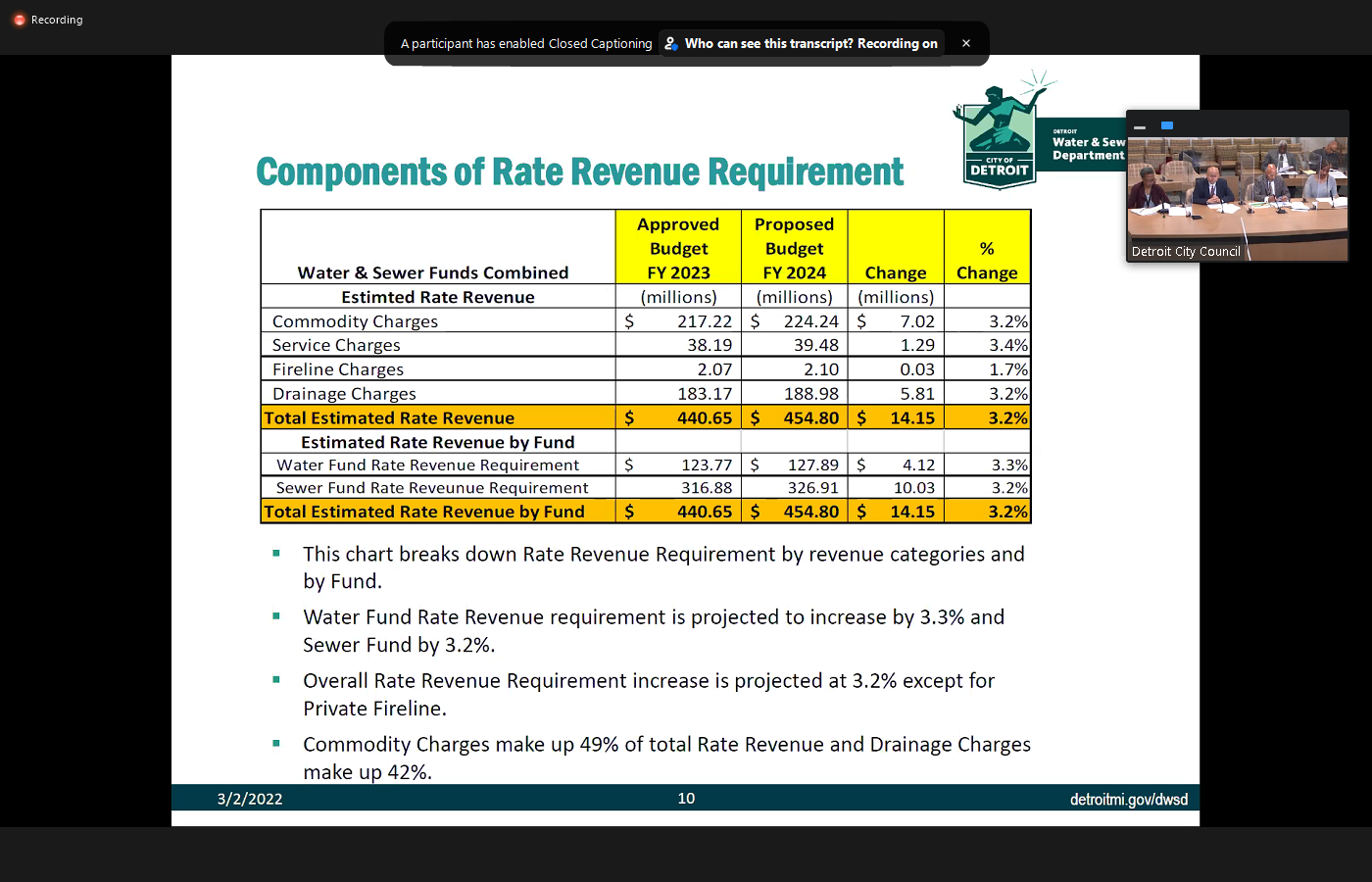

Thank you, Gary. And so I'm going to be brief, giving you an overview of our financing structure, how we come up with the budget. As Gary mentioned, there's this concept of revenue requirements. That's all the revenues that we need to sustain and operate our systems. And really, what does it cost to operate and sustain our system? primarily made of three different components. The first one is called departmental expense. We also call it direct expenses. The second component is non departmental. We termed it as indirect costs. And the third component is revenue finance capital. Now, if you look at the slide, which is slide four, you'll see departmental or direct expenses have increased 6.7% whereas non departmental expenses have decreased by 2.6%. And I'll explain that a little bit later. Revenue finance capital also decreased by 76.5%. The revenue requirement is also broken down on this slide between water and sewer funds. So you can see the water fund revenue requirement is decreasing by 2.9%. Whereas the sewer revenue requirement decreased by 1.6% when we compare it to fy 23. The next slide is just a graphical presentation of what really makes up our revenue requirement is  obvious from this chart, the departmental expenses make up only 22% of our overall expense structure. Departmental expenses, as I mentioned is direct expenses. These are expenses over which DWSD has some as control in terms of increasing decreasing and managing it and that represents $103 million. The big orange chunk you see here, here is the non departmental expense. These are indirect expenses, over which DWSD has very little or no control and I will go through the what makes up those non departmental expenses later a little bit later in this presentation. The chart here is important to show you how much of the overall revenue requirement is what we control. So the slide here is the first component of our cost structure has departmental or direct expenses. And you can see here these are natural classification of expenses, salaries, wages, benefits, contractual services, and so on so forth. And it's, it can see that personal costs making up salaries and wages and employee benefits make up 55% of the total $6.5 million increase here. And then a $5.2 million increase in personal costs represents 81% of the total increase. It also represents 16.8% increase over fy 23. This increase is mainly due to increase in projected FTEs for FY 24. Majority of the projected FTE increases are in our operations cost center. And that's in order to address our strategic initiatives to improve our service levels as well as to address backlog in service deliverables. The next slide the non departmental or indirect cost, where I said that we have little or no control. These are the components that make up the non departmental charges. You look at wholesale charges which is controlled by GL WA, B bifurcation that that that existed before we bifurcated into two different organizations. Post bifurcation that would be debt that we incurred after we separated then it also include bad debts and some other costs such as BNC notes and IWC replica contribution. So on this slide, you'll see that there's a decrease of $10.2 million and this decrease as Gary mentioned earlier, is mainly due to the 35 and a half million dollars, decrease in pension costs. And just to give you a brief background here, when we bifurcated from the bifurcated between GL WB and as GL WA, which is a Great Lakes Water Authority DWSD and the city of Detroit Retirement System entered into an agreement where we were required to contribute $45.4 million to the pension system for our employees. Now here, our share was $13.5 million out of this 45.4 and GL wsa was 31.9. This agreement is ending on June 30. Of this year, and starting with July 1 of 2023 and for next fiscal year and future years, the liability the pension liability will be determined by actuarial valuation and not just an agreement. So for 24 We don't have that previous agreement agreed upon obligation, but we have included $10 million in our in our budget for FY 24. Again, as I said, GL who has the major share in this they share 70% of this so they will be contributing $7 million and we DWSD will contribute $3 million to this part. Other increases and on the chart is a wholesale charges which is increasing again due to DWSD is sharing GL ws revenue requirements. And it's all based on calculation of water demand, including volumes and peak period demands, as well as some buffer that GL wa incorporates into the calculation. The new calculation gives us a share of 12.39% versus 11.9888%. And in the past, overall GL ws increase in revenue requirement resulted in a 6.2% wholesale charge increases and then the sewer fund increased by two point the third big component of this non departmental increase is post verification that that relates to that that we issued after bifurcation. You'll see it this big increase because in FY 23 This course was included in our improvement and extension fund. Which is also known as the ISP plan. Starting with fy 24. We have moved this cost to the O nm cost structure so that's that's why you'll see zero

obvious from this chart, the departmental expenses make up only 22% of our overall expense structure. Departmental expenses, as I mentioned is direct expenses. These are expenses over which DWSD has some as control in terms of increasing decreasing and managing it and that represents $103 million. The big orange chunk you see here, here is the non departmental expense. These are indirect expenses, over which DWSD has very little or no control and I will go through the what makes up those non departmental expenses later a little bit later in this presentation. The chart here is important to show you how much of the overall revenue requirement is what we control. So the slide here is the first component of our cost structure has departmental or direct expenses. And you can see here these are natural classification of expenses, salaries, wages, benefits, contractual services, and so on so forth. And it's, it can see that personal costs making up salaries and wages and employee benefits make up 55% of the total $6.5 million increase here. And then a $5.2 million increase in personal costs represents 81% of the total increase. It also represents 16.8% increase over fy 23. This increase is mainly due to increase in projected FTEs for FY 24. Majority of the projected FTE increases are in our operations cost center. And that's in order to address our strategic initiatives to improve our service levels as well as to address backlog in service deliverables. The next slide the non departmental or indirect cost, where I said that we have little or no control. These are the components that make up the non departmental charges. You look at wholesale charges which is controlled by GL WA, B bifurcation that that that existed before we bifurcated into two different organizations. Post bifurcation that would be debt that we incurred after we separated then it also include bad debts and some other costs such as BNC notes and IWC replica contribution. So on this slide, you'll see that there's a decrease of $10.2 million and this decrease as Gary mentioned earlier, is mainly due to the 35 and a half million dollars, decrease in pension costs. And just to give you a brief background here, when we bifurcated from the bifurcated between GL WB and as GL WA, which is a Great Lakes Water Authority DWSD and the city of Detroit Retirement System entered into an agreement where we were required to contribute $45.4 million to the pension system for our employees. Now here, our share was $13.5 million out of this 45.4 and GL wsa was 31.9. This agreement is ending on June 30. Of this year, and starting with July 1 of 2023 and for next fiscal year and future years, the liability the pension liability will be determined by actuarial valuation and not just an agreement. So for 24 We don't have that previous agreement agreed upon obligation, but we have included $10 million in our in our budget for FY 24. Again, as I said, GL who has the major share in this they share 70% of this so they will be contributing $7 million and we DWSD will contribute $3 million to this part. Other increases and on the chart is a wholesale charges which is increasing again due to DWSD is sharing GL ws revenue requirements. And it's all based on calculation of water demand, including volumes and peak period demands, as well as some buffer that GL wa incorporates into the calculation. The new calculation gives us a share of 12.39% versus 11.9888%. And in the past, overall GL ws increase in revenue requirement resulted in a 6.2% wholesale charge increases and then the sewer fund increased by two point the third big component of this non departmental increase is post verification that that relates to that that we issued after bifurcation. You'll see it this big increase because in FY 23 This course was included in our improvement and extension fund. Which is also known as the ISP plan. Starting with fy 24. We have moved this cost to the O nm cost structure so that's that's why you'll see zero  in 23 but 17.4 $8,000,000.24. moving on quickly here again a chart will show you that the wholesale charges make up the bulk of our cost structure followed by pre bifurcation and post bifurcation there. Again, these are costs over which DWSD has very little, little or no control. How do we find our revenue requirement? We have rate revenue or also as non rate revenue that makes up our retail revenue structure. And then we also have non retail revenue. The charges gives you an idea of how much rate how much of the cost that we need to operate wouldn't be covered to rate revenue, non rate revenue as well as non retail revenue. So the question that that comes up in the front is why is there a decrease in revenue requirements but increasing rate revenue is the bottom part of the chart explains that so we take our entire rate revenue requirement, and then cert and non retail revenue needs to be backed out from a rate revenue in order to arrive at rate revenue requirements. That's why you will see revenue requirement as a whole has decreased by 2%. But our rate revenue has increased by

in 23 but 17.4 $8,000,000.24. moving on quickly here again a chart will show you that the wholesale charges make up the bulk of our cost structure followed by pre bifurcation and post bifurcation there. Again, these are costs over which DWSD has very little, little or no control. How do we find our revenue requirement? We have rate revenue or also as non rate revenue that makes up our retail revenue structure. And then we also have non retail revenue. The charges gives you an idea of how much rate how much of the cost that we need to operate wouldn't be covered to rate revenue, non rate revenue as well as non retail revenue. So the question that that comes up in the front is why is there a decrease in revenue requirements but increasing rate revenue is the bottom part of the chart explains that so we take our entire rate revenue requirement, and then cert and non retail revenue needs to be backed out from a rate revenue in order to arrive at rate revenue requirements. That's why you will see revenue requirement as a whole has decreased by 2%. But our rate revenue has increased by

3.2%. Components of rate revenue what makes up our rate revenue structure is commodity sales which is a volume volumetric sale for water sewer. And then we have service charges and then to other components in terms of wireline charges in our water fun and drainage charges in our sewer fund. As you will see this estimated read rate revenue increases 3.2% for both the proposed rate structure is on the slide here. We are keeping our rates at three less than 3.5% definitely less than 4%. You will see the water volumetric rate is 3.3% for both the tiers as we implemented an inclining block rate starting in FY 23 and our service rate is at 3.3. Similarly for our sewer our volume rate is capped at 3.1%. And our service rate at 3.1%. Range charges is even below that we're targeting 2.5% increase in our drainage charges. The next two slides I don't think I want to go through this just a backup of how we come up with the revenues and what water expenses are in. At the bottom of that you will see the difference which is called Total Revenue finance cash flow. I just want to go to the last slide here. Give you a sense of our FTAs as I'm as we mentioned earlier, we have are increasing our FTE there are 58 new positions we we are targeting for FY 24 And mainly all in operations with the sole objective of improving our service levels as well as to reduce our backlog and service deliverables. That kind of concludes my presentation. We'll be more than happy to answer your questions.

3.2%. Components of rate revenue what makes up our rate revenue structure is commodity sales which is a volume volumetric sale for water sewer. And then we have service charges and then to other components in terms of wireline charges in our water fun and drainage charges in our sewer fund. As you will see this estimated read rate revenue increases 3.2% for both the proposed rate structure is on the slide here. We are keeping our rates at three less than 3.5% definitely less than 4%. You will see the water volumetric rate is 3.3% for both the tiers as we implemented an inclining block rate starting in FY 23 and our service rate is at 3.3. Similarly for our sewer our volume rate is capped at 3.1%. And our service rate at 3.1%. Range charges is even below that we're targeting 2.5% increase in our drainage charges. The next two slides I don't think I want to go through this just a backup of how we come up with the revenues and what water expenses are in. At the bottom of that you will see the difference which is called Total Revenue finance cash flow. I just want to go to the last slide here. Give you a sense of our FTAs as I'm as we mentioned earlier, we have are increasing our FTE there are 58 new positions we we are targeting for FY 24 And mainly all in operations with the sole objective of improving our service levels as well as to reduce our backlog and service deliverables. That kind of concludes my presentation. We'll be more than happy to answer your questions.

+1

obvious from this chart, the departmental expenses make up only 22% of our overall expense structure. Departmental expenses, as I mentioned is direct expenses. These are expenses over which DWSD has some as control in terms of increasing decreasing and managing it and that represents $103 million. The big orange chunk you see here, here is the non departmental expense. These are indirect expenses, over which DWSD has very little or no control and I will go through the what makes up those non departmental expenses later a little bit later in this presentation. The chart here is important to show you how much of the overall revenue requirement is what we control. So the slide here is the first component of our cost structure has departmental or direct expenses. And you can see here these are natural classification of expenses, salaries, wages, benefits, contractual services, and so on so forth. And it's, it can see that personal costs making up salaries and wages and employee benefits make up 55% of the total $6.5 million increase here. And then a $5.2 million increase in personal costs represents 81% of the total increase. It also represents 16.8% increase over fy 23. This increase is mainly due to increase in projected FTEs for FY 24. Majority of the projected FTE increases are in our operations cost center. And that's in order to address our strategic initiatives to improve our service levels as well as to address backlog in service deliverables. The next slide the non departmental or indirect cost, where I said that we have little or no control. These are the components that make up the non departmental charges. You look at wholesale charges which is controlled by GL WA, B bifurcation that that that existed before we bifurcated into two different organizations. Post bifurcation that would be debt that we incurred after we separated then it also include bad debts and some other costs such as BNC notes and IWC replica contribution. So on this slide, you'll see that there's a decrease of $10.2 million and this decrease as Gary mentioned earlier, is mainly due to the 35 and a half million dollars, decrease in pension costs. And just to give you a brief background here, when we bifurcated from the bifurcated between GL WB and as GL WA, which is a Great Lakes Water Authority DWSD and the city of Detroit Retirement System entered into an agreement where we were required to contribute $45.4 million to the pension system for our employees. Now here, our share was $13.5 million out of this 45.4 and GL wsa was 31.9. This agreement is ending on June 30. Of this year, and starting with July 1 of 2023 and for next fiscal year and future years, the liability the pension liability will be determined by actuarial valuation and not just an agreement. So for 24 We don't have that previous agreement agreed upon obligation, but we have included $10 million in our in our budget for FY 24. Again, as I said, GL who has the major share in this they share 70% of this so they will be contributing $7 million and we DWSD will contribute $3 million to this part. Other increases and on the chart is a wholesale charges which is increasing again due to DWSD is sharing GL ws revenue requirements. And it's all based on calculation of water demand, including volumes and peak period demands, as well as some buffer that GL wa incorporates into the calculation. The new calculation gives us a share of 12.39% versus 11.9888%. And in the past, overall GL ws increase in revenue requirement resulted in a 6.2% wholesale charge increases and then the sewer fund increased by two point the third big component of this non departmental increase is post verification that that relates to that that we issued after bifurcation. You'll see it this big increase because in FY 23 This course was included in our improvement and extension fund. Which is also known as the ISP plan. Starting with fy 24. We have moved this cost to the O nm cost structure so that's that's why you'll see zero +1

in 23 but 17.4 $8,000,000.24. moving on quickly here again a chart will show you that the wholesale charges make up the bulk of our cost structure followed by pre bifurcation and post bifurcation there. Again, these are costs over which DWSD has very little, little or no control. How do we find our revenue requirement? We have rate revenue or also as non rate revenue that makes up our retail revenue structure. And then we also have non retail revenue. The charges gives you an idea of how much rate how much of the cost that we need to operate wouldn't be covered to rate revenue, non rate revenue as well as non retail revenue. So the question that that comes up in the front is why is there a decrease in revenue requirements but increasing rate revenue is the bottom part of the chart explains that so we take our entire rate revenue requirement, and then cert and non retail revenue needs to be backed out from a rate revenue in order to arrive at rate revenue requirements. That's why you will see revenue requirement as a whole has decreased by 2%. But our rate revenue has increased by +2

3.2%. Components of rate revenue what makes up our rate revenue structure is commodity sales which is a volume volumetric sale for water sewer. And then we have service charges and then to other components in terms of wireline charges in our water fun and drainage charges in our sewer fund. As you will see this estimated read rate revenue increases 3.2% for both the proposed rate structure is on the slide here. We are keeping our rates at three less than 3.5% definitely less than 4%. You will see the water volumetric rate is 3.3% for both the tiers as we implemented an inclining block rate starting in FY 23 and our service rate is at 3.3. Similarly for our sewer our volume rate is capped at 3.1%. And our service rate at 3.1%. Range charges is even below that we're targeting 2.5% increase in our drainage charges. The next two slides I don't think I want to go through this just a backup of how we come up with the revenues and what water expenses are in. At the bottom of that you will see the difference which is called Total Revenue finance cash flow. I just want to go to the last slide here. Give you a sense of our FTAs as I'm as we mentioned earlier, we have are increasing our FTE there are 58 new positions we we are targeting for FY 24 And mainly all in operations with the sole objective of improving our service levels as well as to reduce our backlog and service deliverables. That kind of concludes my presentation. We'll be more than happy to answer your questions. Speaker 10

Directly well I just want to point out that going through two years of COVID had a devastating effect on everybody will glow international pandemic and DWSD in order to stay within budget did not replace a lot of employees that retired. Deferred a lot of work that should have gone on but now that our we're out of the COVID situation. We have our finances in order. The only concern I have is the bad debt as you see $60 million in bad debt and 23 $60 million in 24. That's because of the moratorium. We were collecting it 94% of what we build prior to the moratorium. And so we're confident that with the new Lifeline program in place and with the governor signing a supplemental budget agreement for $25 million, in which DWSD is confident we're going to try to capture the lion's share of that the governor also put in the new budget for this starts in October, another $45 million, which total $65 million to fund the Lifeline program at least in play for DWSD. We've gone to all of our legislators and the governor's office and said basically, if you We appreciate the 45 million but if you make that 75 million plus the 25 supplemental budget that's 100. And we won't need to come back and ask for any additional funds for the four years that you're in office. And so that was favorably received. We're hoping that you'd support that and also express that interest to our state legislators that when the state's budget gets approved, if we could move from 45 million to 75 million that would secure the funding source for lifeline for the next four years. And with that said I can address any issues with regards to lifeline or any other questions that you might have.

President Sheffield

Thank you so much director Brown in actually was one that particular program but you just addressed the sustainable or the sustainability of the program. With funding. So I will hold that question. And I want to talk a little bit about the water basement backup program. From my understanding that is through ARPA, I understand it's not in the budget but as to ARPA funding. I'm just curious as the rollout for other neighborhoods to be included. I know that we have phase one and phase two, we identified 11 neighborhoods. I'm just curious as the overall need in general city wide for the program, and I know different areas experienced more flooding than others. But I think that there are still other pockets of the city that had issues with water and flooding and so can you just speak to the overall vision of how we plan to properly fund with ARPA funding this particular program which is very popular, and the overall money that is going to be set aside for it.

Speaker 10

I'll be glad to thank you, man. I've received the text since I've been been sitting here there's $800,000. That's on an open PIO, currently that we're going to be able to utilize and within the next couple of days, put the plumbers to work on approximately 133 homes all in the Jefferson Chalmers area that will in the dollars that were made available for the pilot program. We certainly learned a lot in that program. Originally we did not allow the plumbers to do work on the outside of the house. They only could do it on the inside the scope of service we've since been told that the CFO of the city is going to move $4 million into the basement backup program. And so you're going to be asked I believe I'm asking the law department to make it an emergency to bring new contracts that will change the scope of work and give the customer the option. If they don't want their basement torn up. They can do this work outside. That would be one of the changes and we will also implement some of the things that we learned during this process. So we have $4 million to continue the basement backup program. As you will recall, the program only allocated work to be done in 11 neighborhoods and there's certainly a lot more neighborhoods around the city that need that that work done. I'm expecting within the next 60 days to be notified by FEMA that they will contribute a another $4 million on top of the forming dollars of ARPA money to be utilized. And so we're hoping to be able to finish the commitment of the 11 neighborhoods. And then as we keep coming with all of our projects to look for additional funding, we would like to expand it throughout the city to other areas that weren't initially but right now what I have in hand is or what what's what's coming in the next couple of days the contracts is $4 million. Barbara money. And then i i I'm not even cautiously optimistic. I've we've been made aware from FEMA that it's just a matter of time, but we'll get another $4 million for the program. I can tell you that it's extremely successful. One of the things that we learned in the program is that a third of the basement that we put a camera in before we put the backwater valve on the lateral sewer line has separated from and so we are also cautiously optimistic that we're going to be awarded $47 million to do lateral sewer lines. And so instead of telling the customer as we are now that we can't move forward because your line has fallen off, the $47 million will be used for a lateral sewer line program, both inside the basement backup program and customers that are not receiving backflow preventers, but just need a need to have their line reconnected to the system. There's $7 million that should be made available for that. So you should once that money arrives we'll try to get the those contracts won't be hard to put to put together we'll we'll put them together. Similar to the basement backup program where we're using Detroit based plumbers, we may need to go out and try to find some larger companies to be able to go faster because the seven or eight now are small companies and we need to the one thing that we learned is we're going to need at least two larger companies that can take 100 homes at a time and be able to move a lot faster because for sure it will start raining in the spring and people will have problems and we want to get as many of these these homes done as we can

President Sheffield

additional 4 million that is coming in arpa. Is that within the 11 already identify neighborhoods or is it going to be able to be extended outside of that

Speaker 10

we have 2000 customers in the love it neighborhoods, okay and the total of the money we've spent now and the 4 million plus the four from FEMA would not cover all of its simple math. Six $6,000 per home, divided into $4,000,000.02 and we have 2000 homes to do so that won't even get us halfway

President Sheffield

Why is the goal not then if it's simple math to add more ARPA funds to address the outstanding issues of the resident, the 2000 that we've identified that need the

Speaker 10

help. Oh, I'll be I asked was much much.

President Sheffield

Simpler. It seems very simple. Yes, yeah. Yeah. Yeah, I'm glad so I definitely want to make sure we put that into the Executive Session, because I know, the mayor has indicated that the ARPA amendment will be coming with the budget so we can talk about both of these issues at the same time. And so is there a motion to add that to Executive Session motion? All right, Hearing no objections, we will add that and then my last question, because I know I'll submit the rest of the writing page six. It says that the majority of the projected FTE are in the operations cost center to help improve service levels as well as to address backlog in service deliverables. Yeah, what what are your major backlogs? Right now?

Speaker 10

Restorations Okay. Restoration one we're gonna talk over the last two years during COVID When we were losing people and trying to stay within budget and not we didn't want to lay anyone off, but we certainly weren't replacing people. We got behind in restorations. You know, I'm happy to report that I don't think anywhere in the country, as a city put 6000 new meters on homes that have come online. A lot of them are land bank properties that are coming online and that's that's a really good thing, but we need more people to be able to do our that type. of work.

President Sheffield

Okay, so how many FTEs then are going to be hired and this is just for restoration of property that was damaged.

Speaker 10

It's 24, I believe, and this is for field service technicians they can work in and what we call our maintenance and repair sections, if you call them and have a hydrant that's an issue, this team that we also calls sinkholes. We also will be getting contractors on board to help get caught up on the sinkholes as well as the restorations but the 24 fsts are for maintenance and repair along with meter operations. And then we're going to be hiring another 40 fsts that we won't be using rate dollars or budgeted dollars that you're approving a day but we've been approved by what source of funding is that? We've been approved by $5 million from what's the source of funding for the the FST that we're hiring for the letters. Yes. Yeah, we got we got almost $90 million. We committed to this body that we would take fighters that's not coming out of the budget dollars. But is Tucker has authorized HR to begin the hiring those 42 letters line work. And I'm sorry, it's our goal to be able to get them to do the work cheaper than contractors and then force the price down from contractors.

President Sheffield

All right. Thank you. We have several questions. We'll put them in writing. And looking forward to your response. President Pro Tem things

Speaker 12

like Madam President, there we go. Thank you, Director brown being here. You and your team. Appreciate you always being responsive. We'll see you this Saturday as well at the Dima muffling meeting with folks who learn about 10 o'clock. A whole host of things. Yes, sir. 10 o'clock regarding DWSD. So appreciate that. Madam president hit the question. I was going to ask about the restoration. So thank you for that. So I'll just be brief with this other question that we learned about during the Department of Administrative Hearings, budget hearing and they indicated that the billing disputes are no longer being held at D H. They were now back with you all are with the waterboard, what was the rationale for moving them from waterboard to gauge and then moving them from d h back to Waterloo? That's always a question folks. Like, Hey, hold on, you got one telling me basically adjudicating their own bills and their own disputes.

Speaker 10

Yeah, it did. It was it was my idea to move it out from under DWSD and get some independent magistrates, if you will, the same people that do the administrative hearings, to to hear those cases and hopefully be more transparent about how, how they were being handled. I'm gonna have to get back to you on it, you know, and I can do it in writing as to why we moved it back. But I know that there was a backlog and some other issues that went on where they weren't being done timely. I certainly don't want to indicate that that was on administrative hearings. I really believe it was on my team side of of the ledger, but I can get back to you in writing on what the rationale was for bringing it back and and if we can work out something that can make it more independent on I think I'm with you on being transparent and having an independent magistrate look at look at these cases as opposed DWSD hate hearing officers, if you will. But that sounds like my general counsel who

Speaker 13

filled the chair. We we made the decision to but actually the most common reason for billing disputes is unusually high usage on a bill. And what we did was we we met with constituents we met with the DH at length. What we determined was, a lot of times people have a leak in their home and they have an unusually high bill and they dispute the bill saying that the meter must have broke, but we can see from their usage that there was some sort of leak and we can tell that by during the midnight to 3am hours, there's water running, which indicates a leaky toilet. So what we did was we implemented two new policies, the leak adjustment policy, which allows the customer to come in and say you know, there's there's a leak in my house, diagnose the leak, and we will give them they don't need to dispute there. They can seek and it's been repaired. We will count there will Seward's charge is reduced. Yes they use the water but if it just if it just ran flee, they will receive a discount because it was not so that has to be treated. It was just clean water. If they had a leak perhaps on the outside of their home, a spigot and the water just ran into the grass, they will get an even greater adjustment on their bill. So it was a more customer friendly way of not making them have to file a dispute and go through the DH we just handle it on the front end with the customer, which has been utilized many times by customers. They've been very we've gotten a lot of good feedback on that. The other thing we've enacted was a meter accuracy dispute policy. If you think there was no leak, and you think there was something wrong with our meter, then we can have the meter tested. And if the meter shows some sort of defect then they will their bill will be adjusted based on prior usage. And we will install a new meter. If the meter is found not to be defective. Then you know we will let the customer enter to payment plan. We'll also work with them to double check if there were any leaks in the home. So it was it was twofold. It was to be more customer centric and try to work with the customer on the front end so they didn't need to go through the DH for dispute plus the DH charges $50 To hear every dispute and oftentimes the disputes were for less than $50. So we will work with customers and maybe adjust their bill. If you know we can't determine what it was but it's certainly less than the $50 administrative fee. So sorry for the long answer, but the intent was to be transparent and more customer centric with this policy change.

Speaker 12

I appreciate that. I mean it's good information. The transparency part still though is is something that's always caught called into question when the department that you're having a dispute with is the one who's actually adjudicate the dispute as well. So I appreciate though the dispute the media accuracy, dispute policy, as well as the discounts offered very worthy products that you have. But again, we're hearing just from folks on the other end and you know, maybe it's oversized complaints about it, but you know, just from the outside looking in, it makes sense to have a third party who would even outside of those disputes that you all are able to address right then and there. There are probably other types of different disputes that would benefit I think from a level of transparency and a third party so

Speaker 13

I'm buds bins office is always a recourse. For someone who feels like they have not received fair treatment from the water department. And the ombudsman's office, you know will work with them. They'll act as a as a neutral arbitrator for any disputes as well.

Speaker 12

You said that the majority of the disputes are less than $50

Speaker 13

that I'm saying quite often they were less than $50. So it wasn't worth paying the $50 to the DH to to arbitrate something. But for things that were larger, we found it was primarily due to leaks that occurred in the home.

Speaker 12

You have no right to have more conversation. Yeah, thank you. Again, I'm Martin garden restoration and we have others that we might ask as well. In the interest of time, I'll yield the floor. Thank you.

Unknown Speaker

Thank you Thank you. Councilmember waters. Thank you.

Unknown Speaker

I am Good afternoon.

Speaker 14

I really don't have that much Madam President that acts all of the questions. Okay, anyway. I just

Speaker 15

want to inquire about your, your federal grant process. You pretty aggressive going after the federal grants for water infrastructure and so forth.

Speaker 10

I was on a federal call with Health and Human Services at noon today. Regarding going after additional dollars for our lifeline plan, we've received $100 million for from the federal government for LED service line replacement and we are aggressively reaching out to state and federal sources along with grants from foundations to improve our system. So we are extremely aggressive. We have a team of of people that work on that, Dan. All right.

Unknown Speaker

Well, thank you. Thank you, Madam President. Thank you so much member waters, and member Doha.

Speaker 16

Thank you, Madam President. Good afternoon. I have a couple of questions. One of my questions already asked by council president as well, relative to the basement backup protection plan, which is something that's in district seven and District Four. remember walking out there with you with Michael Regan from the EPA and it was just a program where parts of residence at Aviation subdivision we're really excited about you have you and I've had multiple discussions on how we expand that we do with that. And so it's been getting rave and hopefully we'll see this summer. How much of the flooding will be made as well. But again, thank you for that and for the discussions on that and ways that we can expand it. One of the questions I have is something that people call in about all the time, which is stormwater or drainage fees, right. And there's also always some questions because folks don't understand how that works. Why am I getting charged for that? Why, you know, so my question is kind of twofold. One, what are we doing to try to work and help educate better or educate our residents better on why they're draining this fees? are high. And this is not just residential, this is commercials as well we get calls from churches. And the second thing is, what can we look at? Where are some ideas? We can look at the Hellgate that yeah, and maybe you know, obviously some of it and you and I have discusses infrastructure right and not just infrastructure underneath the ground or bus or on our on our part should I say, but infrastructure relative to driveways and sidewalks that may belong to private residence or private commercial businesses or driveways that may be there was really a resonance. What's that educational component look like? And how are we going to work to try to mitigate that or just provide more information on how residents themselves can mitigate that to brain drainage fees down I mean, the

Unknown Speaker

dura ux by for question.

Unknown Speaker

But, but it's all wrapped in well,

President Sheffield

I hear you I know I just want to make sure we are we're behind so we can everyone. Okay, thank you. And

Speaker 10

so I won't. I can spend an hour talking about how we got to the drainage rate methodology that we have, but let me just say that is Tucker hired a company called Stantec to do a rate study. And the study came back and basically said we were charging too much of our services on the sewer side of the house as opposed to water side of the house. So we moved, I believe $20 million last year from sewer which sewer the sewer charges are half times the rate of water. So when you move $20 million out of sewer into water you're automatically reducing overall rates for residential customers especially. And then we change the complete way in which we do our rates to an inclining block rate methodology, meaning the customers that use the least amount of water residents on average, three to 4000 gallons a month. On average. They pay less and the customers like Marathon Oil or some of the big industrial customers that use a lot of water, pay more and that was a way to make sure that we were being sensitive to our residential customers that are we're struggling to pay the bills. And so a lot of what we what we have done to reduce rates didn't go directly toward the drainage charge, but we reduced charges on water and sewer to reduce the overall bill. So you know, we're sensitive to the fact that we have a $680 Approximately drainage charge per acre. And we're, we're also the I don't think I mentioned it earlier, but for many years prior to the bifurcation DWSD had double rate increases, sometimes as high as 17%. A year. That's unsustainable for residential customers. As you heard me say, the last eight years we've averaged 2.8 less than 3%. And so I you know, that's what I tried to tell our customers that we're doing everything that we can to reduce your cost and of course, whenever you do that, there are winners and losers and the high water users are feel like they're losers and I have a meeting next week with some of the industrial customers that are saying the residents aren't paying enough. They paid more we paid less and of course, you know how you know where that conversation is going. It's it will have it, respect their opinion, but we're going to try to do everything we can to reduce costs for residential customers within legal bounds without being sued and and that's what we're doing.

Speaker 16

Okay, my second question, I'll be very quick. I know we had a hearing at 3pm. We're about 11 minutes behind relative to Rouge Park and those projects that are happening. I was happy to stand with you. We are now 75 million. Just want a quick update on that. Yeah, and where that is rerouting that water to the roof

Speaker 10

and we're ahead of schedule. You know, we said that was going to be a four year project. The contractor came and I you know, I went out and promised the residents that every year we would clean up we would we would not leave an open street similar to what happened in Rosedale was that the grief? The grief I received there, rightfully so. We learned our lesson so I put it in the contract. If you open up the street at the end of the year, if you don't finish you have to and the contractor came back to us in this case in the far west project and said if you let me work through the winter, I'll finish this project in three years because of escalating inflationary cost. He was going to see a great amount of savings. So we're well ahead of schedule and I'd be glad to send you have Lisa Wallach send you an update on the progress. We just had a meeting I think last week my team met with we were started Mr. Ed wasn't there we always look forward to seeing him at that particular meeting. But we're well ahead of schedule now. And the complaints are way down from the project. I did in Roseville. Well, I'm sorry, apologizing for that. We're gonna go back and he's gonna have me at a meeting on Saturday.

Speaker 16

For folks who have told me about the project priority.

Speaker 10

Yes, that's the thing about going first, you know, we did one project on the west side, one project on the east side, we learned a lot. But we got we got things wrong that we corrected, going forward. So we apologize, but we're going to try to do better as we as we know better.

Speaker 16

We appreciate that. Obviously, I have more questions. I know we have restraints and time. This is one of the most important departments that residents call about every single day. But I will submit the rest of my questions after this, so thank you very much, Madam

President Sheffield

Thank you. And just to be clear, too, we can still move the entire budget into the executive session and we can have the director come back address any outstanding questions or concerns that are raised at this table. We just do have another department that is waiting after. However, if there are urgent questions that we want to as a body address now, we can do that. I'm just trying to make sure that we stick within our one hour is not to be mean or to come across in any way. I just want to make sure we are sticking within our within our one hour budget hearings. So member Johnson.

Speaker 17

Thank you Madam President. And good afternoon. Good afternoon. So I want to ask a question relative to something that you brought up that you mentioned the bad debt expense, roughly $60 million. Is all of that from residential customers. None from commercial.

Speaker 10

The majority of it is yes. From residential. Yeah, I mean, they're they're, you know 240,000 Roughly residential customers, the 22,000 commercial customers and for the most part, they are we sue them when they don't pay their bills. We don't sue residential customers. We have a lot more tools and handles to collect. So yes, but I can assure you that the Lifeline program is going to quickly get us back into the, you know, into the 93 94% collection rate,

Speaker 17