Loading...

Community Land Trust 101: Laying the Groundwork in Hamilton County

Andrea Davis

Thank you for joining us today. I'm Andrea Davis, Executive Director of hand and I'm excited to welcome you to the first in a new series of spin offs following the 2025 suburban housing conference. At the conference, we shared a wide range of ideas and tools to address housing challenges in our communities. We also asked for your feedback, and this topic community land trusts was one that stood out. So we're kicking off the series today with today's webinar to take a closer look. Thanks to Jim Morris, who will be joining us shortly, Michael Osborne and Carol Gassen for joining as panelists this morning. We have more than 40, I'm sorry, more than 80 people registered today. So it's clear the interest in this conversation is strong. Video from grounded solutions, the grounded Solutions Network, so that we're all kind of on the same page about what a community land trust is. This is a short video that kind of explains the basic concept. So bear with me while I flash back to 2020 and remember how to share screens and all that good stuff, and we will get rolling, maybe,

Speaker 1

community

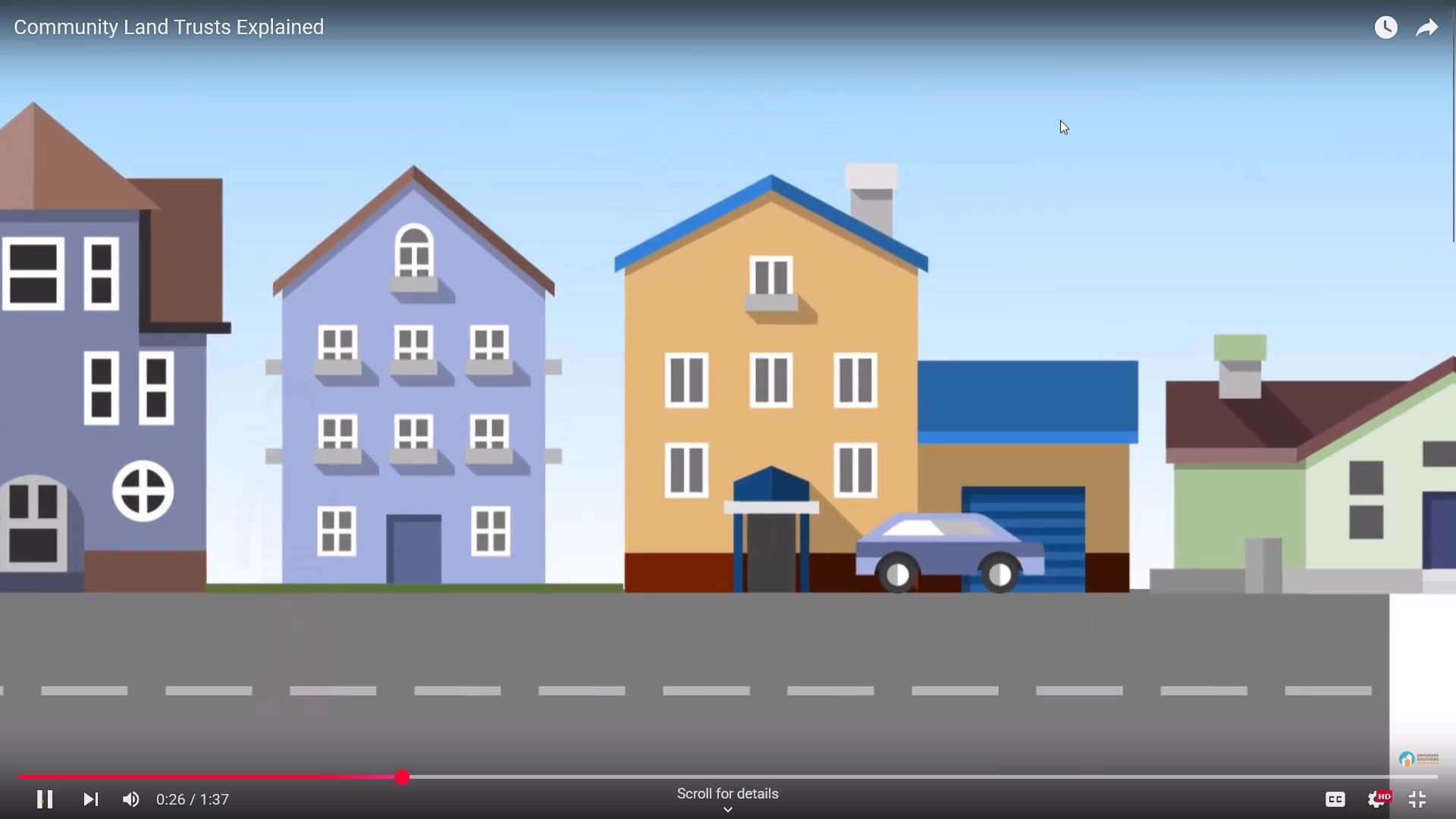

land trusts, or CLTs, are non profit organizations that acquire own and steward land permanently for the common good. The most common CLT land use is housing, but retail office and a variety of other uses are possible. CLTs give formal decision making voice and power to local community residents in determining land uses. Here's how CLTs make home buying affordable for families in their communities. First, the CLT builds or buys homes using one time public or private investment. Next, the CLT sells just the home to a low income buyer who qualifies for a mortgage, and the CLT keeps the land, holding it in trust for future generations of home buyers. In return for being able to buy a home at a discounted price, the family agrees to pay it forward and sell to another low income family at a price they can afford. The CLT manages the sales process, ensuring that each home buying family builds some wealth from a predetermined limited amount of the sales proceeds in this way, the one time public or private investment in CLT homes makes lasting affordability a reality and stabilizes communities. And CLTs benefit the larger community too, as they

land trusts, or CLTs, are non profit organizations that acquire own and steward land permanently for the common good. The most common CLT land use is housing, but retail office and a variety of other uses are possible. CLTs give formal decision making voice and power to local community residents in determining land uses. Here's how CLTs make home buying affordable for families in their communities. First, the CLT builds or buys homes using one time public or private investment. Next, the CLT sells just the home to a low income buyer who qualifies for a mortgage, and the CLT keeps the land, holding it in trust for future generations of home buyers. In return for being able to buy a home at a discounted price, the family agrees to pay it forward and sell to another low income family at a price they can afford. The CLT manages the sales process, ensuring that each home buying family builds some wealth from a predetermined limited amount of the sales proceeds in this way, the one time public or private investment in CLT homes makes lasting affordability a reality and stabilizes communities. And CLTs benefit the larger community too, as they

preserve and protect housing for long term residents, helping to build stronger, safer and higher quality, diverse neighborhoods, contributing to greater educational attainment, employment opportunities and health outcomes. Visit ground solutions.org to learn more about CLTs today.

preserve and protect housing for long term residents, helping to build stronger, safer and higher quality, diverse neighborhoods, contributing to greater educational attainment, employment opportunities and health outcomes. Visit ground solutions.org to learn more about CLTs today.

+6

land trusts, or CLTs, are non profit organizations that acquire own and steward land permanently for the common good. The most common CLT land use is housing, but retail office and a variety of other uses are possible. CLTs give formal decision making voice and power to local community residents in determining land uses. Here's how CLTs make home buying affordable for families in their communities. First, the CLT builds or buys homes using one time public or private investment. Next, the CLT sells just the home to a low income buyer who qualifies for a mortgage, and the CLT keeps the land, holding it in trust for future generations of home buyers. In return for being able to buy a home at a discounted price, the family agrees to pay it forward and sell to another low income family at a price they can afford. The CLT manages the sales process, ensuring that each home buying family builds some wealth from a predetermined limited amount of the sales proceeds in this way, the one time public or private investment in CLT homes makes lasting affordability a reality and stabilizes communities. And CLTs benefit the larger community too, as they

+2

preserve and protect housing for long term residents, helping to build stronger, safer and higher quality, diverse neighborhoods, contributing to greater educational attainment, employment opportunities and health outcomes. Visit ground solutions.org to learn more about CLTs today. Andrea Davis

There you have it, thanks to our friends at the grounded Solutions Network. As many of you know, housing costs in Hamilton County have been rising faster than wages for years, making it harder for working families, young professionals and older adults to find a home they can afford, and the need is growing. According to the latest Alice report from United Way, one in four Hamilton County households that's more than 35,000 households are either living in poverty or are considered Alice, or are considered Alice, asset limited, income constrained and employed essentially, are working poor. These are working families who earn too much to qualify for federal assistance, but not enough to afford the basics, things like housing, child care, food, transportation and health care,

Andrea Davis

but still falling behind. Today's conversation is about one tool that can help change that, and how we're working together to bring it to life. This session is focused on the Hamilton County Community Land Trust, or CLT, an initiative being developed by members of the Hamilton County Housing collaborative, a group of local nonprofits, government partners and funders who are working together to create more housing options across the county. The CLT is designed to ensure that homes, whether for rent or for sale, stay affordable, not just for the first resident, but for all future residents. It's a big idea, and one that depends on deep collaboration. Before we dive into the backstory, I want to be clear the Hamilton County Community Land Trust is not a hand initiative, but a community driven effort because hand convenes the housing collaborative. We've taken on responsibilities like applying for funding to help move the work forward on behalf of the group, but this effort belongs to the collaborative. I'm honored today to be joined by a few of the key partners helping make this possible. Michael Osborne from i three community housing solutions, our consultant who helped develop the CLT model and secure early funding. Jim Morris, who I need to figure out how to admit to the meeting here, from greater indie Habitat for Humanity, and he also helped shape the initial collaboration. Also Carol Gassen from Merchants Bank, who brings the banking perspective and will share why financial institutions are supporting this work. I'll also be sharing some reflections from Han's role as convener and partner in this process. Over the next hour, we'll walk through how this idea started, how we're building the model, and what it will take to launch. We'll also leave time for questions and share ways you can get involved. Let's start by looking at how this idea took root and how collaboration made it possible.

Andrea Davis

Carol and Michael, you both have been part of the housing collaborative. Can you share a little bit about, you know, how this idea sort of rose to the top for the group.

Speaker 2

Well, sure, I'll, you know, one of the things that's been really great is that we had the opportunity to come together and have listening sessions and really put ideas and constructive, thoughtful, thinking together to help develop what might become a very solid Housing Strategy and just Overall, making the community better happening.

Speaker 3

I think the originally I wasn't involved, but in 2022 I think it was a county housing study was done by hand on behalf of the collaborative, and that's the CLT was identified as one of four priority tools or initiatives to seriously address this. And so at that point, though, it was in concept, these four things make sense, right? Here's a CLT across the country. They seem to be doing a good job. It seems like it might be a fit here. We ought to consider it as it were, right? So I think then, in my role was then engaged by hand to kind of do local due diligence, if you will. You know, to move from concept to what would one in Hamilton County actually look like? How would we fund it? What could it do? Etc. Because that's, I think that the video did a great job. Here's what the concept is, right of CLT, but everyone, and there's 300 and some across the country, every CLT is really sort of adapted to its local circumstances and priorities and needs, etc. So my role at that point in 2023 was really to kind of do community engagement, get identify those opportunities, needs direction, and build kind of a framework again, of what a specific Hamilton County CLT would look like.

Andrea Davis

Let's jump to you know how CLT kind of basic explanation, but tell us a little bit more about you know, how this tool really does preserve affordability and,

Speaker 3

yeah, yeah. Well, specifically, again, the video highlighted that housing and home ownership is really something nearly all CLTs are engaged with. But you know, we shouldn't think narrowly that that's the only thing the CLT could or would ever do. But in terms of, you know, its focus, it's clearly home ownership. And at the core of the CLT model is that separation of land and improvements, the ownership separated ownership of land and improvements. And as it mentioned, you know, there's a formula, ultimately that's agreed upon by the CLT, established by the CLT and the homeowner that says, you know, we will, we will provide this homeownership opportunity to you at we'll say, below market value, right? You'll be able to buy $300,000 home for $200,000 to make it affordable in the future, then by a predetermined formula established for the whole CLT, not homeowner by homeowner. It says in the future, when you decide to sell, and you can decide anytime you want when you decide to sell, here's the maximum affordable price you would pay it forward with to use the term. Now, you know the formulas can be very different. Different structures will serve different purposes, but that's the core of how it preserves affordability, because upfront, someone gets the benefit of affordable home ownership, and then knows down the road, they will pass it along or Pay It Forward affordably as well.

Andrea Davis

Now you said something like you the buyer would pay $200,000 for a $300 house, as if he were bought a $200,000 house, but sale price of the house actually is still that full market value, right?

Speaker 3

It's still, well, it's still, the formula would still track what's the full market value of the land and the improvements, and as we anticipate it here, the formula would continue to be tied to that. So someone would pay 210 $200,000 let's say that may have nothing to do with the value of the improvements themselves, because it maybe not $100,000 lot, right? But subsidy goes in the buyer would would buy would mortgage. They turn to Carol and need a $200,000 mortgage, right? They'd have a 99 year lease on the land at 20 or 30 or 40 bucks a month, right? So they've got control of the land and the improvements, and lenders will loan a smaller mortgage that's affordable to this home. The

Speaker 3

in the future, there is this, you're still tied to that $300,000 house down the road becomes 400,000 but that homeowner can't sell it for 400,000 on the open market. They have to sell it to another eligible buyer at now, we'll say now 300 is affordable, right? So there's this initial subsidy that makes it affordable, and then through the CLT mechanism, it keeps it affordable forever. Essentially,

Andrea Davis

that's a long time compared to, you know, the work that hand does. We receive subsidy to help with construction costs to build rental housing, and in exchange for that assistance, we agree to keep our rents affordable for, you know, a certain period of time, typically 1520, or 30 years. So you know, to have affordability kind of perpetual is really kind of a kind of the secret sauce, right? Because,

Speaker 3

yeah, and I will quickly say too, on in my prior home ownership development. Yeah, absolutely, only the time frame for affordability was shorter. So we would do development. We'd provide that $100,000 subsidy into the project. Five years later, potentially, that homeowner could now sell the home that they bought it to. They could sell it for full market value at 400,000 to anybody they wanted. So either the public sector, you know, local government, writes another big check to re subsidize the next buyer, or you've lost that affordable unit you've created,

Andrea Davis

right, and that initial $100,000 investment is

Unknown Speaker

just goes away. Yep, yep.

Andrea Davis

You mentioned, you know, we've talked about CLTs as a tool in our toolkit, kind of maybe a Swiss Army knife of a tool, because it can be, you know, deployed in so many different ways. Is there a particular, you know, toothpick or tweezer that better in suburban markets like ours, then, you know how a CLT might work in a more urban area going through, you know, blight and that

Speaker 3

stuff, yeah, well, one, one way would be, you know, CLT is that work in, we say, more distressed neighborhoods, typically, maybe an urban area, they're much more focused on supply they need. Nobody else is developing. They need to develop, I would say, in in not just in Hamilton County, and that's it's very applicable here, but other suburban CLTs focus more on the demand side, because there's plenty of development occurring so so, you know, here in Hamilton County, we'd anticipate that really a core of this CLT programming would be a Homebuyer Assistance Program. And it works where buyers get subsidy, get assistance to go out and buy a home on the market where they want the kind of home they want, you know, otherwise, the CLT helps make it affordable, and in the process of that person buying the home, it gets slid into the CLT. And in the suburbs this sort of approach. I mean, not only is it good from a market standpoint, but here in Hamilton County, I think it really is applicable because it allows folks the choice of location in a very diverse county, right, the choice of housing type in a diverse county of school district, it's not like it's a monolithic place, right? So it really this sort of approach in the suburbs is really adaptable to the diversity that can occur in suburbs, in product and geography. You know, you live close you want to live close to work, you want to live in a particular school district, or you want a blue house or greenhouse or right? So that's really applicable here where there's where supply is not a problem. It's truly the demand. It's the affordability that needs to be

Andrea Davis

absolutely and that sort of gets at one of the challenges hand has in developing rental housing. You know, when we go into a community, we often have to battle the NIMBY pushback, right? Not in my backyard. If you've attended any of our events, you know, we have the NIMBYs, and then also the notes, which are not over there either. And then, of course, my favorite, I have to give credit to Bruce accordingly, from pedcor, every time I say it, the bananas build absolutely nothing anywhere near anything the you know, and that's because when we're going in, we're building multiple units, you know, together in a community. Typically, you know, it may be as few as four, four or five units, it may be as many as 60, but we're definitely people know we're there, and they know who our population is. And there's this perception or stigma that folks who need affordable housing, you know, we don't want them as neighbors. It's going to increase crime and traffic and all sorts of things. I think as hand has done its work, we've, you know, started to change minds about that. I don't think you know many of our residents are creating problems in their neighborhoods. But what I really liked about the CLT Homebuyer Assistance model is, you know nobody you know a house is for sale on your block, and a low income a homeowner buys it through the CLT. Nobody needs to know what financing mechanism was used to acquire that home. I mean, if you think about you know your neighborhood, you don't know you just know you have a new neighbor. And to be able to eliminate that stigma and that, you know, people thinking, every time they drive by a neighborhood, oh, that's where the poor people are really a remarkable opportunity,

Speaker 3

or the or that the product is very low quality, either, I mean, yes, buying on the open market, what Joe and Mary private seller are selling, right?

Andrea Davis

Yeah. And in other markets where you see more like redevelopment, we've seen some redevelopment. In Hamilton County, I think our housing stock

Andrea Davis

like neighborhoods disappearing and being redeveloped very much yet. But in in areas where that is happening, CLT s have been used to sort of keep existing housing housing, instead of, you know, kind of being subjected to the bulldozer, which is kind of special, but let's transition and away from, you know, kind of the the the program details, and think a little bit about how this kind of fits in big picture. Carol Merchants Bank has been very supportive of the CLT concept. From the beginning, we were fortunate to partner with you all to apply for a grant to help support the Hamilton County CLT startup, and thank you so much for helping make that happen. But tell us a little bit about how merchants you know has been involved in this, and why it's something that you all see is as a priority for you.

Speaker 2

Well, at our company, we are putting affordable housing, whether that be through multifamily or single family, and we're headquartered right here in Hamilton County. So it is really important to us to make sure that where we have our headquarters and where a lot of our employees live and also work here, that we provide quality affordable housing for people that are our neighbors. And so we knew that it was really critical for us to engage. And of course, in looking across the landscape, we can see that hand is very much a leader in terms of providing alternative solutions for affordable housing. And so leading on into this grant program. When we got word that the Federal Home Loan Bank, who is often making grant programs available for home buying and home repair,

Speaker 2

Indiana and Michigan, they developed this new program, the community multiplier program, which allowed for distribution of dollars to eligible organizations that were providing certain things for their communities, one of which was the CLT. And so we decided at the very moment that we got word of this grant, because the dollars were limited, we knew that we wanted to come together and come to the table with hand and so work to get the application submitted. And we're fortunate enough to be able to get that done timely. And we did receive the award together, so it was a $50,000 contribution from the Federal Home Loan Bank, and also a requirement that the bank match at 10% So $55,000 was allocated then for support of legal form.

Speaker 2

And governance, development, program design, and so all of you attendees today are kind of witnessing this process as it's unfolding and the standing up of this great idea.

Andrea Davis

Well, thank you so much for your support. Is that, as has merchants worked with land trusts in other markets. I know, you know, obviously you're not just here,

Speaker 2

right? So we are actively engaged in Marion County also, and that is up and coming, and we've got a representative from our bank on the board there, and hope to see that really flourish and do good things there, too.

Andrea Davis

Excellent. I know you know, having we noticed a lot of employees are registered for the for the webinar today, I think, in kind of talking about the Community Land Trust out in the community, I've noticed, you know, lenders seem to Get it a little quicker than than some other kind of civilians, I guess, is, is there anything about the the CLT model versus, you know, the many other opportunities I know merchants has, you know, been a lender in hand projects, and I'm sure You know, many other affordable housing initiatives. Is there anything about the CLT in particular that kind of resonates more than than anything else? Or

Speaker 2

Yeah, so I want to really turn the question a little bit to what Community Reinvestment Act officers do at local banks. We obviously have an obligation to serve the low to moderate income needs of our communities,

Speaker 2

and so we have formulated a Community Reinvestment Act, CRA Indiana Bankers Association, which brings together CRA officers and community development personnel from across the state, and we meet periodically and talk about different ideas that will help us all make our communities better and stronger. It you know, it takes all of us working together, and we often call it coopetition, because, you know, banks are friendly in this space, and although we still want it to be able to land a deal and make a loan, so we come together and look at all the different options and consider the benefits of different programs. And one of the key things about a CLT is it is innovative in the way that it comes together and also is distributed housing, often and so like, right? And while you're talking about the benefits of having this type of home in a neighborhood that is undetectable as being affordable, that's a beautiful thing, and so you're making an impact. You're helping a local family be able to afford a house, a beautiful home, and be able to stay there and contribute, then to their community too. So as CRA officers, we're looking for a variety of ways that we can engage and of course, our regulators look at our performance in lending, investments and services. And so there are ways that we can work with the CLT on all those angles, with making a loan for that home buyer that you mentioned earlier, when they're ready to buy that home, we can

Speaker 2

CLT With that public investment that we talked about, or private investment, I mean, so there are different tools that we can do direct contributions or different types of investments with EQ to type of investments that could be then deployed to help The organization or CLT buy up those land and those properties to then pull into the CLT, and then, of course, services where we can volunteer on boards and or work with home buyers, for example, providing financial literacy education and and the like.

Andrea Davis

I think it's important, you know, you mentioned the mortgage. A CLT mortgage is different than your standard. You know, I I saw a house and I made an offer on it mortgage because the land and the and the improvements are separated, so it really just takes gender to be able to to deal with that. That said, despite the fact that merchants, bank is, you know, kind of in on the ground floor of the Hamilton County. CLT, it sounds like there's still an opportunity for other lenders, other banks, to sort of jump on board and help promote this, right? You're not

Speaker 2

absolutely, yeah, and you know, it's only the beginning. So this is a long term strategy that I think anyone who has a branch in Hamilton County ought to be thinking about. Yeah, we should be there and engage in any way to help raise all boats. Really is what we're after here.

Andrea Davis

Sure,

Speaker 3

let me. Let me add something that ties in a little bit. Another key element in the CLT is not just this structure of separated ownership of land versus improvements, but also again, CLT is in it for the long term, right? Forever. So different than traditional ownership, affordable home ownership, the CLT has a very robust stewardship program forever as it relates to its portfolio, the CLT needs to steward the property itself, right that there's mechanisms to make sure that the property is maintained, kept up, etc, etc. Because they share the equity of it, they make the steward. And this is kind of spurred by Carol's comment, they're stewards of the family as well, to make sure that the family is successful and builds wealth. And can they stay or they can build wealth and move on, right? And and they steward the public investment that goes into it. So there's there's real to borrow from, like social services. There's kind of wraparound services involved. It's not just we'll put the CLT provides an affordable opportunity, and then, you know, done, moves on. CLT is in it with the public investor, with the property and with the homeowner, family forever and

Speaker 3

I won't have touted it, but I've read a number of studies as recently as 2019, 2020, that actually show, for instance, the rate of delinquency and foreclosure of CLT homeowners is dramatically, half or lower the national average. So these are, frankly, good mortgages to make, too from a just from a lending security standpoint,

Andrea Davis

because of those,

Unknown Speaker

yeah, because that stewardship, yes,

Speaker 2

that's fair well, and for lenders to engage. You know, we did our homework to determine at our company, for example, we originate to sell to the agencies Freddie and Fannie, and we have explored the opportunity there to make those that possible. And they do accept that, so we can continue with operating under our current model. And then also these homebuyers as low income or moderate income homebuyers to still utilize other programming for funding or financing that would allow them to make that home that much more affordable with down payment assistance, some through the Federal Home Loan Bank too, and then other different tools that are available to those first time home buyers, for example. So there are a lot of different ways that we can put this puzzle together and have success.

Andrea Davis

Absolutely like it's the Swiss Army Knife effect, Legos, swiss army knife. You know, we can, let's, let's talk a little bit about this, the governance and the structure and the community involvement in the CLT. I'm going to try to share my screen again, just to kind of help our

Speaker 2

our view

Andrea Davis

Ah, so Michael, do you want to talk a little bit about, you know, sort of where we are, where we go from here, and you know how the governance structure and community involvement really works?

Speaker 3

Yeah. Well, I'll start with sort of the governance structure. I think that's probably a good segue here. I mean, it is true to its name. It is a community land trust, right? I mean, it is a separate nonprofit that has a community based board. And in fact, the typical, the typical model for CLT boards, and in fact, HUD now even mandates, if you want to receive HUD funding, it has to be this. The membership has to the membership has to elect the directors that can't all be appointed, and 1/3 of the board are literally, in this case, 1/3 of the board would be people who own CLT homes and have leases with the CLT so, I mean, that's very direct the program, right? So 1/3 of the board would be the people who are in the program. Another one through the board has to be people either who are residents of the area of operations, in this case, Hamilton County, or representatives of businesses or institutions that are that serve Hamilton County, and then the other third of the board. Oh, and I think this is laid out in the middle of the slide that's in front of you, the other third of the board really are representatives of kind of the greater public interest that's served by the CLT. So, you know, units of government could, could have representation, housing policy, or housing, other housing related entities, but it's very much community based, and that's the model that works the best, and like settings even mandated in some cases.

Andrea Davis

Gotcha it and it makes sense, right? It's a it's a community.

Andrea Davis

Explicitly, when the, when the land trust is established, it will be its own separate 501, c3, nonprofit.

Speaker 3

Did  you want to talk about some of these other engagement opportunities? Or, yes please, well, or if you liked it, you can, I guess the, you know, the process of standing up the CLT, frankly, from we've got a framework. Here's generally what it should look like, how would operate, etc. But now it's time to fill in all the blanks, right? So it's for a while it's going to be focused on program development, you know, creating the details of that Homebuyer Assistance Program and creating the kind of the infrastructure, if you will, with needed for any kind of homeownership programming. So the the the lender documents, the ground lease document, setting that resale formula, getting all of that stuff, getting into the weeds, getting all that stuff settled. Here's the program that's a good six month effort, to be honest with you. Then when, as that nears completion, then it's time to sort of build out the governance part, and that's where you'll see. You'll go from an organizing committee that's providing the sort of technical input and helping shape policy decisions early, you'll go from that to the full board of directors. Then the CLT will exist as a corporate entity. It'll have members, and anybody out there on this call can join, right? So it's an open membership, but it'll have a board of directors that'll happen, you know, in, let's say, the second half of the year long process. And to go back to the engagement part as well, it's anticipated that there would be, although maybe a, you know, nine or 10 or 11 member board of directors that's not going to really represent the diversity of stakeholders in the community. So the framework includes having a community advisory council, 20 or 30 people appointed by the board, in some cases, sort of having dedicated seats for certain entities, but having a much broader, diverse community advisory council, required by the bylaws, in fact, that have the opportunity to provide ongoing input and guidance to the board in decision making. So you know, there is, there is community connection all along the process. I would say lastly, then again, it's kind of the second half of the year long effort is really standing it up operationally. Again, not only the governance in place, but like any good endeavor, it needs to have a work program, a budget. You know, what's the five year plan for growing this thing, right? And what's the funding needed, and then going after that funding, and I think it would be good sure to

you want to talk about some of these other engagement opportunities? Or, yes please, well, or if you liked it, you can, I guess the, you know, the process of standing up the CLT, frankly, from we've got a framework. Here's generally what it should look like, how would operate, etc. But now it's time to fill in all the blanks, right? So it's for a while it's going to be focused on program development, you know, creating the details of that Homebuyer Assistance Program and creating the kind of the infrastructure, if you will, with needed for any kind of homeownership programming. So the the the lender documents, the ground lease document, setting that resale formula, getting all of that stuff, getting into the weeds, getting all that stuff settled. Here's the program that's a good six month effort, to be honest with you. Then when, as that nears completion, then it's time to sort of build out the governance part, and that's where you'll see. You'll go from an organizing committee that's providing the sort of technical input and helping shape policy decisions early, you'll go from that to the full board of directors. Then the CLT will exist as a corporate entity. It'll have members, and anybody out there on this call can join, right? So it's an open membership, but it'll have a board of directors that'll happen, you know, in, let's say, the second half of the year long process. And to go back to the engagement part as well, it's anticipated that there would be, although maybe a, you know, nine or 10 or 11 member board of directors that's not going to really represent the diversity of stakeholders in the community. So the framework includes having a community advisory council, 20 or 30 people appointed by the board, in some cases, sort of having dedicated seats for certain entities, but having a much broader, diverse community advisory council, required by the bylaws, in fact, that have the opportunity to provide ongoing input and guidance to the board in decision making. So you know, there is, there is community connection all along the process. I would say lastly, then again, it's kind of the second half of the year long effort is really standing it up operationally. Again, not only the governance in place, but like any good endeavor, it needs to have a work program, a budget. You know, what's the five year plan for growing this thing, right? And what's the funding needed, and then going after that funding, and I think it would be good sure to

+1

you want to talk about some of these other engagement opportunities? Or, yes please, well, or if you liked it, you can, I guess the, you know, the process of standing up the CLT, frankly, from we've got a framework. Here's generally what it should look like, how would operate, etc. But now it's time to fill in all the blanks, right? So it's for a while it's going to be focused on program development, you know, creating the details of that Homebuyer Assistance Program and creating the kind of the infrastructure, if you will, with needed for any kind of homeownership programming. So the the the lender documents, the ground lease document, setting that resale formula, getting all of that stuff, getting into the weeds, getting all that stuff settled. Here's the program that's a good six month effort, to be honest with you. Then when, as that nears completion, then it's time to sort of build out the governance part, and that's where you'll see. You'll go from an organizing committee that's providing the sort of technical input and helping shape policy decisions early, you'll go from that to the full board of directors. Then the CLT will exist as a corporate entity. It'll have members, and anybody out there on this call can join, right? So it's an open membership, but it'll have a board of directors that'll happen, you know, in, let's say, the second half of the year long process. And to go back to the engagement part as well, it's anticipated that there would be, although maybe a, you know, nine or 10 or 11 member board of directors that's not going to really represent the diversity of stakeholders in the community. So the framework includes having a community advisory council, 20 or 30 people appointed by the board, in some cases, sort of having dedicated seats for certain entities, but having a much broader, diverse community advisory council, required by the bylaws, in fact, that have the opportunity to provide ongoing input and guidance to the board in decision making. So you know, there is, there is community connection all along the process. I would say lastly, then again, it's kind of the second half of the year long effort is really standing it up operationally. Again, not only the governance in place, but like any good endeavor, it needs to have a work program, a budget. You know, what's the five year plan for growing this thing, right? And what's the funding needed, and then going after that funding, and I think it would be good sure to Speaker 3

there's a deliberate component of community engagement once, once you can sort of say, here's what it is, right? You have something to show. Then there needs to be a real, there will be a real, deliberate and aggressive effort to get out into the community and say, here's this tool, here's this tool, city government. How can it partner with you? How can it help you? Here's this tool, community, neighborhood, here's what it's doing, right? So that's got that will be an important part as well. Knock on wood with with it being funded, standing up, operational, going live late summer to fall of 2026, a year from now.

Andrea Davis

It's definitely a process. It takes a while. The funding is not an insignificant part of that. And thank you again to merchants and Federal Home Loan Bank for kind of giving us a kickstart on that. Michael, as you sort of major round socializing the idea, you know,

Andrea Davis

community stakeholders. I know you spent hundreds of hours, you know, kind of doing that initial outreach. What are some of the lessons that you got from that, that you think will help, you know, kind of build a successful

Speaker 3

Well, I think lesson, or key takeaway, I was one very surprised at the at the level of support and the broad based acknowledgement that, you know, there is a need there. And there was a surprising quick attachment to ooh, this swiss army knife could work right? Different entities saw it in different ways. So the city of x versus the city of y might have seen it in the context of supporting home ownership. Another in terms of, like, gee, we could adapt development standards to incentivize and here's the CLT, other that could help with that. Others saw it in terms of kind of stewarding the public subsidy, right? Here's a tool we're going to invest in, in creating development our community, here's a tool that can help protect it and preserve it, right? So I thought that was that was really quite surprising to me. I think the other, the other takeaways really found themselves into this framework. And I think the home buyer Assistance Program really came out of the feedback of, here's what we need, here's what's going on in the market, here's what we can here's what we can do. So I think that that that reflects what the input was. The last piece that I think was impactful on me in terms of thinking through the framework was, once again, not to be a broken record, but to go back to the diversity, in many ways, the diversity of the County and the area of operations that what it does and where It does it has to be very adaptable, very flexible. Uh, something in partnership with, you know, Sheridan, for instance, and a whole different thing in partnership over here, it needs to be able to deploy itself in different areas, in different ways, with different partners. And that does that. And it sounds very fluffy like, well, wouldn't everybody want to do it? It's a lot more difficult, too, as opposed to working in a 20 square block neighborhood where your role, you know, your reason for being, is one thing. So I think that was that was a lesson that we need to keep in mind as it gets built out. How do you stay flexible, adaptable and able to serve a diversity of this broad, this big County,

Andrea Davis

a diversity of needs really right? Because the needs cured and are different than the needs in Carmel, for example. And so that's where the community involvement in both setting up land,

Andrea Davis

going long term, I think is special because, as I know, it's difficult to get a community to change its mind about something, but if they're already on, you know, if, if they see that the tool that's being deployed is solving the problem that they have, Not a different problem, I think it's a lot, a lot more easily, easy to get on board with. So there are multiple opportunities to get engaged. The folks on this call, I'm going to share my screen again. Bear with me. I'm sorry. You know we do have a funding gap. We have identified the initial cost of getting this started over the one year period to be somewhere around $150,000 we've we've secured 55,000 of that. So we are actively fundraising to support both the operational and startup costs through donations and grant or funder connections. So if any of you can help with that, we most interested. We also, you know, are looking for folks who have expertise in these areas, lending, real estate, outreach, development, legal, you know, all kinds of area of opportunities to plug in

Unknown Speaker

local

Andrea Davis

government, absolutely. You know, those are very important partners and part of the stakeholders. To Michael, did you know reach out to yeah, please feel free to chime in on these. If anyone has, has any others to add, spreading the word, right, like Michael said, you know, engaging with the community and making sure that folks are aware of this program and how it works, and how it works in different communities is really going to be key, not just to the success of the program, but to the success of the people who participate in it. You know these I know because I get phone calls every day from folks who need housing in our county, and I'm just so excited to be able to share another opportunity with them, eventually partner.

Andrea Davis

Next year will be a lot of sort of building of programs and policies and that sort of thing. But it's never too soon to identify land that could be used for a future project funding opportunities, or even projects that could involve the land trust down the road. I know developing affordable housing is a is a long process, and you know, we're starting to think now about how community land trust might fit into our plans five years from now, that sort of thing. So if there are ways you think you might be able to plug in in the future, I urge you to reach out and get involved and just stay stay connected. You know, we, we have been working on this initiative since 2021 is when we first started, kind of post COVID, looking at what sort of policies might help Hamilton County avoid a future housing crisis meltdown we saw in 2008 so Yeah, lots of opportunities to get involved. We do the the housing collaborative tries to meet quarterly. Our next meeting is scheduled for August 21 at 9:30am at the Collaboration Hub and fishers, the Community Foundation's Collaboration Hub. So we hope you can join us there. We will be after this. We're going to have some questions and answers here in a second. But before we do that, I wanted to let you know we will be sending out a follow up email this afternoon with a link to the video we watched this morning. Those of you who were a few minutes late might have missed that. Also, we have a one page info sheet that kind of explains the Community Land Trust concept in a little more detail, in a graphic as well, and also a copy of the webinar today. Our sincere apologies to Jim Morris from habitat, who we were unable to make technology work for so lens. And if that's the worst thing that happens today, I guess we will deal with it. But there is a question and answer kind of button on the bottom of your zoom screen. We we've gotten a couple one. Michael answered, If you want to, you want to address that one? Michael,

Speaker 3

yeah, yeah. There was a question about, is one? CLT usable for just one home? Absolutely not quite the opposite is true. So I mean this one, see CLTs, depending on the market you're in, how aggressive they are, how good they are, etc. I mean, some CLT s struggle to build much portfolio, but realistically, yeah, I mean, a CLT could have dozens, or even 150 or 200 homes in its portfolio right. And also the portfolio could be property on which sits an apartment complex and there are CLTs,

Speaker 3

T owned land or groceries on CLT on land. So it's one CLT with a big port, big into first portfolio.

Andrea Davis

Gotcha, there's another question here about the equity formula. Can you kind of explain?

Speaker 3

Yeah. So yeah, there's a question about was the in my example, $300,000 house gets sold for 200 to the home, like the improvements, get sold for 200,000 in some places, that could be the 100,000 could be the value of the land, right? But that's going to be based on the market. Here we're anticipating, without getting away in the weeds, a sort of formula where the 100,000 would not be tied to the value of the land. It can't be because of the what, what value of land versus affordability here is you can't sort of equate to

Speaker 3

a loan go away now the house is affordable, right? So, so no, the answer, I think Wilbur asked, the answer is, no, that 100,000 would not be the value of the land that would be part of building out. The exact formula is, you know, can we? Can we approximate that or not? Probably it's good not to, in this case too, because again, going back to the diversity of the county, you know, the land value under a house in Fishers or in a new subdivision, is going to be very different than the land value as a proportion of overall somewhere else rural, right?

Andrea Davis

So that 100,000 essentially represents the subsidy,

Speaker 3

right? It's the needed it's, it's the needed subsidy to make it affordable, right? To make the overall package affordable. So it happens to be at that home, and honestly, that home could be sold to a family for $200,000 a different family with a slightly different income maybe ends up buying, buying home ownership for 220 well, so they obviously, they should. They have a greater share in the equity over time of the home, because they were able to buy more, right or afford more. So the approach has to take into account the need to serve this diverse area and have some flexible pricing and subsidization that isn't tied to the land value proper.

Speaker 2

Well, and don't forget that the home owner will build equity as they make their mortgage loan payment. So as they're doing that, you know, the loan amount decreases and their equity increases, so that value will stay with them as they, you know, ultimately choose to move to a different location or stay there for their entire lifetime.

Speaker 3

Yeah, the homeowner actually gets, yeah, the homeowner gets principle they've paid down on their mortgage. Just to put a point to it, as Carol said, the homeowner will get that principle that's paid down they also will share in the growth over time. So when 300 value became 400 They not only got what they paid down on their original mortgage, they get a share of that future appreciation as well,

Andrea Davis

right? And that's part of what will be figured out during the standing up is exactly, is that?

Unknown Speaker

How that needs to work,

Andrea Davis

how that is shared? As Michael kind of alluded to the subsidy on a single on the same home might be different depending on who's buying the house, right? Because it's based on what's affordable based on your income. Affordability is relative, and housing is considered affordable if it represents 30% or less of your gross income. So for one family that $300,000 house is affordable,

Andrea Davis

their family it's affordable at 220 just because they make more. So I think that's important to understand another question here about what was the primary concern or barrier that you encountered as you were shopping the idea around?

Speaker 3

Maybe I was, maybe it was really good at selling the idea, but I'm not sure. I think there. There's certainly a concern or a question around the newness of it. There's a little bit of like, well, we've never heard of this, or there's none around here. Well, Indiana and our market has needed this tool in the toolbox for one thing, right? So I think maybe it may not be a direct answer to your question, but there was that sense of, Well, what? What is wrong with this? Because why? Why don't we have it? Or what hasn't you know what? Right? Have you heard of them before? I think that was probably, that was probably one. And I'm going to, I'm going to use what you asked to jump off to a different topic. I think the real like, so what's not good about it? Well, really, there's nothing that's not good about it if you do it right. And I would emphasize that the real challenge is making sure, for instance, that the the resale formula isn't structured in a way that feels good today, but down the road, all of a sudden, Home Buyers can get out of their homes, or the CLT is on the hook to go get more subsidy for that, for that unit, to keep it affordable, right? So if you don't build it right, it's not going to fly. Well, I know I just jumped from the Swiss Army knife to an airplane, but Right? So I think there, if there's caution around it or suspicion around it, or watch out, here's what's going to go wrong. It's, frankly, in kind of building, right? There's, there's 300 CLT 300 plus CLTs across the country. They they've done it right in different places, right? So they're there. You can adapt the lessons from here. They are there to make it right for you. For Hamilton,

Andrea Davis

yeah, just because we haven't seen it here doesn't mean it. It doesn't doesn't work elsewhere, Michigan, Minnesota, Wisconsin, all have very robust CLT networks. Michael and I actually went to a conference, the Midwest CLT conference, last year to learn more about this. And I was really impressed with how far you know, how much further ahead these communities are, and how they're using these CLTs to achieve their goals. It's really, really kind of cool. Could you all talk a little bit about how property taxes for CLT properties work? You know, I know, Michael, that was something when you were out there, you specifically talked to the assessor's office about, obviously, how it works. Exactly, Will is yet to be determined.

Speaker 3

You know, you know, there was actually pending legislation which could take forever, but it's actually pending legislation to make it very, very explicitly clear how CLT properties are treated from tax purposes right to that says they are homestead right now it's up to a local treasure or local assessor and their determination and interpretation of applying, you know, the homestead credit, the property tax cap, etc. And we did get good feedback in 23 about the concept and the, you know, feasibility of doing that, but there is legislation that would codify. Here's how CLT, the separated land and ownership, has to work, as far as who pays the taxes. I mean, it could be that even structured, either structured many different ways, where in the CLT owner you owner. They they will get a bill. They might get a bill from the treasurer, directly for the improvements, and the CLT gets a bill for the land underneath, right. CLT could build in the monthly ground lease fee, the tax, the property tax cost, right? So it's really the homeowner is going to be responsible for property taxes, the mechanism for, so who literally writes the check? And, you know, is it in the ground lease fee, et cetera, that has to be structured, you know, to be the smoothest, the easiest, the most flexible from that standpoint Sure.

Andrea Davis

Aaron asks, Does the CLT have the ability to work directly with a developer versus an individual home buyer? So in other words, could this be done at scale, as opposed to one onesie? Twosies have been something Jim might have talked about a little bit. So put your Jim Morris hat on.

Speaker 3

So, yeah, absolutely. And that's sort of the that we'll call, kind of the supply side of the equation. The Homebuyer Assistance Program has been, you know, that that's the homebuyer that's on the demand side, people going out looking for other So, yeah, the CL CLT s can work. CLT s can actually be developers, right? Of one home or 50 homes, right? So CLT could be a developer. But here, particularly, there was a there was a couple of units of government that kind of liked the idea of so I think there's some real potential for changes in land use and development standards that incentivize so again, I'll just say city of x can say, hey, private developer, you want to do a 200 unit subdivision. What if we let you do 210 on the same? Right? 10? We'll approve 210 units on the same if you dedicate those extra 10 to the CLT, the builder developer develops and builds the home markets that it gets slid into the CLT at that time of purchase, right? So that mean that's one way you can work with a private developer, where really, they're just doing their thing, but their their numbers work to be able to partner with the CLT through incentives, development, incentives. The other way you could partner, frankly, is if you know the CLT, or in this case, kind of it's, you know, maybe habitat is the developer the CLT and habitat can work together on a habitat development where the properties after habitat develops, then gets the buyers, etc, are then again slide into the CLT for permanent stewardship, right,

Andrea Davis

right? And that is something I know habitat. You know, everyone is familiar with Habitat for Humanity. They build homes. They're actually the mortgage lender as well for their homeowners.

Unknown Speaker

And historically,

Andrea Davis

you know, kind of onesie twosie developments in field development and various lots, but they have habitat in Central Indiana, greater Indy has really started moving more in the direction of acquiring, you know, parcels of land and building neighborhoods that may or may not be completely affordable. You know, there could be some mixed income in there. So in those cases, I think, you know, the affordable units could absolutely fit into a land trust. Whereas market rate units wouldn't necessarily have to to me, like, mixed income neighborhoods are what I remember from my childhood, right? Like, you know, we had a two story next to a one story down the street from a duplex, and that was okay. And I think, you know, I think this would Community Land Trust would kind of allow us to kind of move back in that direction. So let me

Speaker 3

see affordability too. I do want to point out, I mean, I think the other thing that your original housing study even showed,

Speaker 3

ability is not just a challenge for lower income families in Hamilton County. So now some funding for programming is going to be tied to only serving, you know, lower income, but the CLT here needs to be able to assist to some degree and be involved to some degree in helping middle income families, but middle income households achieve home ownership as well. I mean, so again, the the need is broader. So I would, we wouldn't characterize this as it's only for low or very low income families, you know, quasi section eight kind of thing,

Andrea Davis

right? I mean, the reality is, you still have to be able to qualify for mortgage,

Unknown Speaker

right? Yeah, yeah. And

Andrea Davis

that's something, you know, we hand develops rental properties for, for low income, you know, up to 60% of area median income, by and large, our residents aren't mortgage ready, and so we see a unity for to kind of put something else on their housing pathway. But by and large, the folks who are going to get involved in CLTs as buyers, right off the bat, already are mortgage ready, but they just don't have the income to support buying a house at the prices that that you have to pay in Hamilton County to be a homeowner here. So is there anything else before we part? I think we got to most of the questions. There was a question about if, if a, if a an entity that has land believes it could be good for the CLT. Should they be reaching out to hchc? You certainly can. As Michael indicated, you know it's going to take us some time to get the the organization put together and formed, but you know, we don't want to lose opportunities in the meantime either. So

Andrea Davis

or, you know, see what we can do to to perhaps keep it safe, do some safe keeping for the CLT. But, you know, as soon as we are able to kind of put all the pieces together and and get rolling, I think this is really going to be a special opportunity. Swiss Army knife, if you will, for our community. Okay, very good. Any other, any others Michael or Carol that you would like to All right? Well, thank you, everyone for coming today, listening to us, enduring our technical issues. We'll, we'll get better at this before our next webinar. But do look in your emails today for a follow up from Kerri, and if you have any other questions, you know we'll certainly this is a topic we're going to be discussing for quite some time. So we also are available as hand as the collaborative.

Andrea Davis

Anything on Michael's schedule, necessarily, but you know to come and talk to groups and in smaller groups if you want to kind of really dig in in more detail to learn more about the idea and how it might work in your community. So thank you all for your time

Carol Gassen

So there we go.

Andrea Davis

Thanks everyone so much for being here.

Speaker 2

Thank you. Andrea. Thank you.